Some industries have recently faced disruption as their traditional operating models were not flexible enough to maintain their competitive advantages. Many have simply failed to respond to new challenges so others were able to take additional market share.

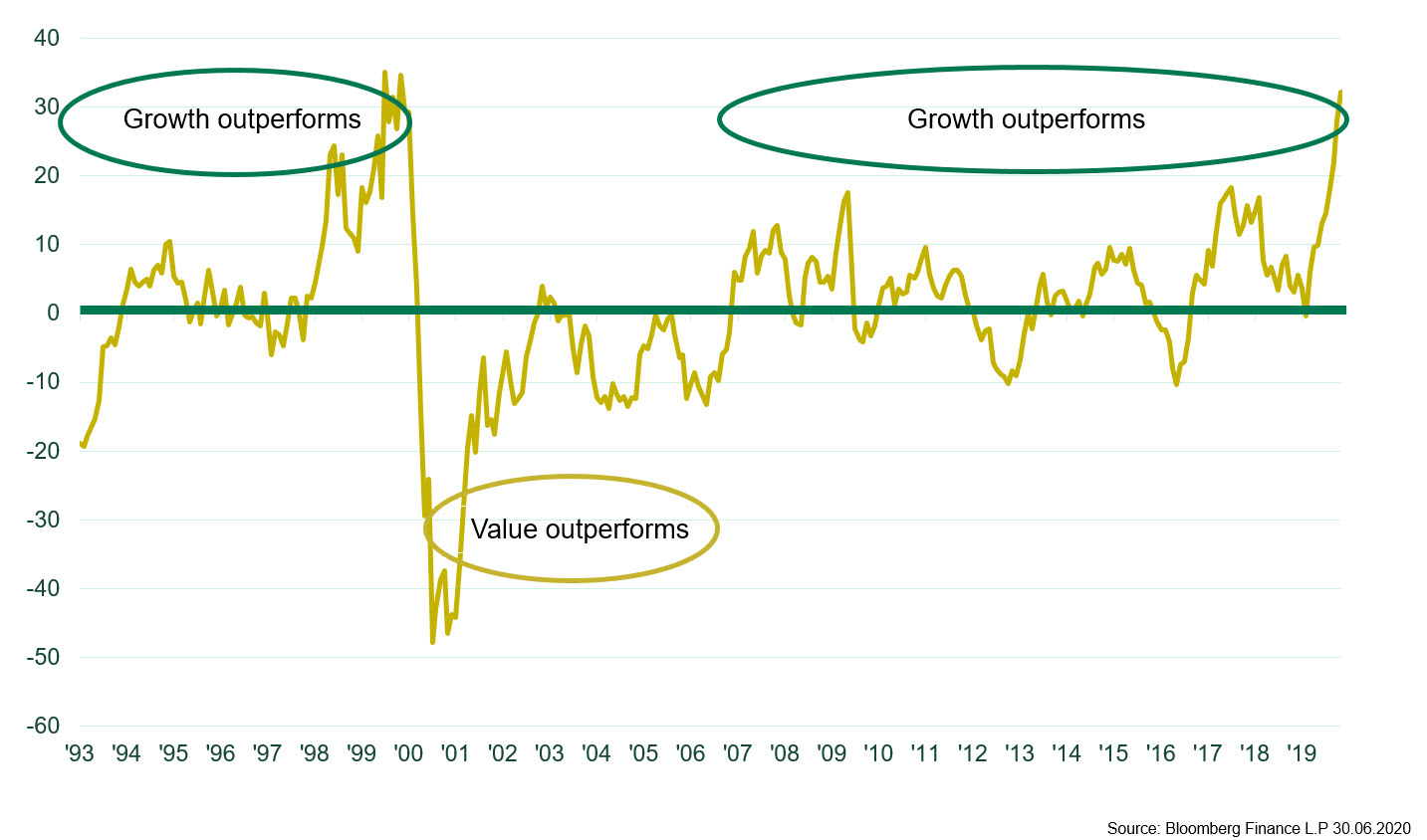

With an economic pie that is not growing, firms need to expand earnings by taking market share from competitors. This phenomenon is amplified by the acceleration in the development and adoption of new technologies, which more growth managers have now invested in. Growth companies have been a consistent performer for almost 30 years (except in the early 2000s) and outperform value companies most of the time.

Opportunities

The US a stable global growth engine

The managers focus on identifying and investing in high-quality, established companies with strong, sustainable business models and competitive advantages. We believe such companies not only have the potential to outperform the market consistently but they also inherently pose less risk. Their superior earnings stability and financial strength provide a safety margin that typically results in less volatility during declining markets or periods of economic or political uncertainty while taking advantage of market growth.

Our quantitative approach to US equities

Within our US equity offering we also provide a long-only, active, systematic stock-picking strategy powered by an external partner’s big data analytics.

The stock selection is based on robust market sentiment signals distilled exclusively from alternative data sources, with a minimum five-year live track record.

Investment process & philosophy

A growth-driven approach with a strong investment process

- Focuses on high-quality companies demonstrating superior and sustainable earnings growth which offer better risk-adjusted returns

- Seeks out companies where valuations have the support of strong earnings per share (EPS) growth and unique business models, while avoiding capital-intensive ones, in order to identify sources of repeatable alpha

UBP applies responsible investment principles across all long-only funds.

A local and seasoned team of specialists:

- Eve Glatt, B. Riley Wealth Management, Senior Portfolio Manager & Co-Head US Equities, has over 20 years of investment experience

- Maurice O. Onyuka, B. Riley Wealth Management, Senior Portfolio Manager & Co-Head US Equities, has over 25 years of investment experience