Market conditions improved during the fourth quarter as investor focus shifted away from trade-related risks and toward the supportive effects of fiscal stimulus and a stabilising monetary policy outlook.

Key Points

- Market conditions improved during the fourth quarter as investor focus shifted away from trade-related risks and toward the supportive effects of fiscal stimulus and a stabilising monetary policy outlook. Risk appetite strengthened into year-end, making 2025 the first year since the pandemic in which all major asset classes delivered positive returns. Equity performance in Q4 remained broad-based but with some dispersion. While emerging markets continued to lead global equities for the year, developed markets advanced in the fourth quarter as confidence improved. Fixed income markets also benefited from improving conditions into year-end as fears of a tariff-driven inflation shock failed to materialise and central banks continued to normalise policy. Performances were positive across the board, supported by attractive starting yields, a weaker USD and tightening credit spreads.

- For the year, performance for the hedge fund industry was very good in absolute terms, but on a relative basis this is a year when a traditional 60/40 portfolio also generated gains of over +13.0%. It was unusual that in a year when equity-related strategies benefited from falling volatility, strategies such as Global Macro - which benefits from higher levels of volatility - also posted healthy returns. With hindsight at year end, it looked to be a relatively easy year to generate gains in a “risk on” environment across most asset classes. In reality though, it was one of the most challenging years as the path between success and mediocrity was unusually narrow for managers.

- In this context, our hedge fund insights this quarter will focus on how market volatility impacted systematic strategies in 2025. Markets initially saw a strong increase both in equity and fixed income volatility, with a clear inflection point on “Liberation Day”, followed by a continuous drop across the board and into year end.

Performance Review

Market conditions improved during the fourth quarter as investor focus shifted away from trade-related risks and toward the supportive effects of fiscal stimulus and a stabilising monetary policy outlook. This followed a volatile first half of the year, when developed market equities experienced a peak drawdown of -16.5% in early April. Risk appetite strengthened into year-end, allowing developed market equities to extend earlier gains and close the year up +19.0%, making 2025 the first year since the pandemic in which all major asset classes delivered positive returns.

For the year, performance of the hedge fund industry was very good in absolute terms, but on a relative basis this is a year when a traditional 60/40 portfolio also generated gains of over +13.0%. It was unusual that in a year when equity-related strategies benefited from falling volatility, strategies such as Global Macro - which benefits from higher levels of volatility - also posted healthy returns. With hindsight at year end, it looked to be a relatively easy year to generate gains in a “risk on” environment across most asset classes. In reality though, it was one of the most challenging years, the path between success and mediocrity was unusually narrow for managers. This is best reflected in the wide spread of returns between top tier managers within strategies. For example, within equity L/S managers - two managers applying the same quality growth philosophy posted over 20 ppts performance difference depending on the relative level of exposure to defence and financial companies. In Global Macro there were opportunities to generate excess returns in EM assets, precious metals & Japanese reflation trades, but if the manager had been forced to cut risk around "Liberation Day", or the summer Quant deleveraging period, then they were struggling to break even for the year. Finally, within multi-strategy we witnessed the comeback of some of the largest managers who had underwhelmed for multiple years.

Hedge Fund Insights: Volatility’s Impact on Systematic Strategies

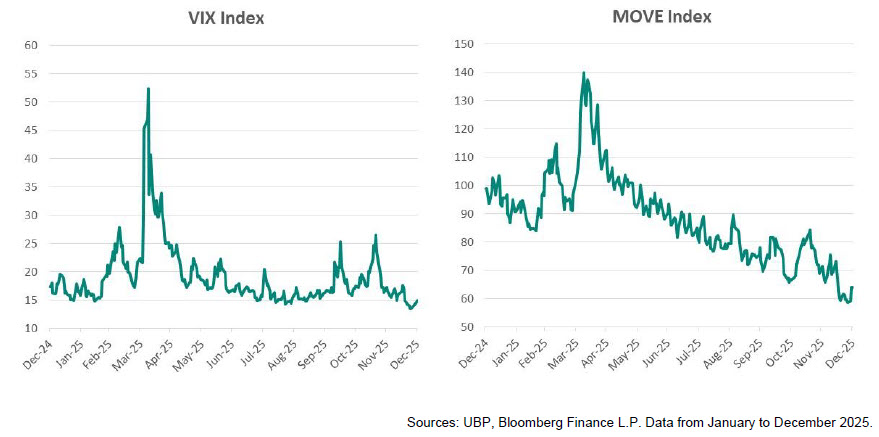

2025 was an eventful year. One of the most interesting features from a market perspective was the evolution of market volatility throughout the year. In summary, the year was split into two periods: Before “Liberation Day” and after. The below charts clearly illustrate that inflection point. In the first part of the year, both equity (VIX Index) and fixed income (MOVE Index) experienced an increase in volatility with a peak during April, and a subsequent large drop. This is particularly notable for fixed income, with the MOVE Index collapsing to multi-year lows in November 2025.

Figures 1 & 2: US equity and fixed income volatility in 2025

While equity markets have rallied strongly since the bottom in April, which is typically the case when volatility drops, fixed income markets have been trading sideways. As a consequence, fixed income markets have been neither directional, which was detrimental to Momentum and Macro strategies, nor volatile, which was detrimental to Short Term strategies. It is very rare for markets to experience both phenomena at the same time.

For hedge funds, this occurrence had a direct impact on performance for systematic strategies in 2025, especially those investing primarily in core markets of fixed income and FX. In H1 2025, these markets suffered from the sharp reversal of prior trends in USD strength and rising yields, followed by limited price breakouts in H2 as volatility compressed. The problem was not that volatility was low, but that it was continuously decreasing. Strategies focused on equity indices and equity factors performed better. However, whilst equity and commodity markets rallied post “Liberation Day” which benefited longer term models, there were pockets of volatility that only lasted a day before reversing which also proved detrimental to shorter term strategies that typically profit from sustained multi-day patterns in these moves.

The question is whether this continues? From a purely statistical perspective, we believe that this is unlikely as implied volatility has reached the levels of the 2010s when central bank policy was stable and accommodative, and could be sustained due to disinflationary pressures. In contrast, heading into 2026, fiscal policy has supremacy with monetary policy relegated to a liquidity support function, against the backdrop of elevated geopolitical risks. This suggests a fertile opportunity in 2026 to trade actively in FX and rates markets that were more muted in the second half of 2025.

Marketing communication. For Professional Investors in Switzerland or Professional Investors as defined by the relevant laws. Past performance is not a guide for current or futures results.

The views and opinions expressed by fund managers (internal or external) may differ from the house view. They are shared for informational purposes and do not constitute investment advice or a recommendation.