In April, we anticipated an inflationary shock and a persistently cautious stance from central banks. That scenario has now materialised, reducing the prospects of any meaningful monetary easing.

However, this has not prevented US and emerging equity markets, particularly Taiwan and South Korea, from reaching new all-time highs. This paradox merits closer scrutiny.

The Middle East conflict has not merely disrupted existing economic equilibria, it has acted as an accelerant for two major transformative forces, namely the race for artificial intelligence (AI) dominance and the reordering of the geopolitical landscape.

Turning to the first of these, substantial investment in AI infrastructure is directly fuelling the global earnings cycle, with the US and Asia at the centre of this technological revolution. For the second, the conflict has laid bare the structural vulnerability of energy markets and accelerated resource nationalism, elevating energy security to a structural investment theme.

Markets are increasingly focused on earnings durability, particularly in sectors directly exposed to AI and energy infrastructure. This dynamic should not, however, mask certain fragilities: elevated sectoral concentration and the pace of earnings re-rating both warrant active near-term risk management.

In fixed income, our scenario of positive returns of 5–6% in 2026 now rests more squarely on carry. We favour emerging market debt, where yields remain attractive, ratings continue to improve, and fundamentals remain solid. Elevated commodity prices provide an additional tailwind, strengthening the fiscal and external positions of resource-rich economies and broadening the fundamental case for the asset class.

Equities remain the core asset class, with a preference for the US market, technology, and sectors linked to electrification and energy security. We also maintain our allocation to gold, whose secular cycle is strengthening, underpinned by structural central bank demand and the diversification of international reserves. In a world undergoing a profound reorganisation, the ability to manage risk actively will be the decisive differentiator.

Key messages

- Earnings over geopolitics

Markets are reaching new highs on the back of resilient corporate earnings, particularly in technology, despite ongoing tensions in the Middle East. - Exceptional AI capital expenditure (capex)

Massive capital investment by US technology companies in AI infrastructure is directly fuelling the global earnings cycle. - Fixed Income

Expected returns of 5–6% in 2026 are driven by carry rather than rate cuts. - Preference for emerging market debt

Attractive yields, improving credit ratings and solid balance sheets underpin our conviction on this asset class. - Two structural themes

AI and energy are no longer sources of transient volatility, but structural drivers of portfolio construction. - Allocation: US technology, energy, gold

The preference is for US equities, technology and energy, with gold maintained as a long-term structural theme.

Our investment stance

Equity markets reaching new highs despite Middle East uncertainty and Brent crude above USD 100/bbl may appear counterintuitive. The current rally reflects the strength of the earnings cycle, particularly in technology, where artificial intelligence continues to drive a major acceleration in investment, revenues and profits. The scale of AI-related capex remains exceptional, with the largest US technology platforms expected to invest heavily again in 2026 and beyond, directly benefiting the global equity earnings cycle. The result is that markets are looking past the geopolitical shock and focusing on the durability of corporate earnings, especially in the sectors most directly exposed to AI, infrastructure and energy. This explains why equities have remained supported even as the oil shock has increased macroeconomic uncertainties. In our view, investors should stay invested for the medium to long term, but may use option strategies to manage shorter-term downside risks and navigate a more volatile geopolitical backdrop.

For fixed income, the outlook is increasingly being driven by carry rather than duration. We continue to expect positive returns of around 5–6% in 2026, but the contribution is likely to come primarily from yields and credit income rather than falling rates. The persistence of high oil prices and the inflation risk linked to the conflict in the Middle East reduce the probability of an aggressive Federal Reserve (Fed) easing cycle, especially as the economy remains resilient. Credit spreads have also compressed back to below pre-conflict levels, suggesting that corporate bond markets are already pricing in a relatively benign outcome from the conflict, while selectivity is necessary to assess the impact of higher energy prices. We continue to favour emerging market debt, where yields remain attractive, and fundamentals are solid. Emerging market (EM) sovereigns show a positive trend in rating actions, while EM corporates have maintained leaner balance sheets than many of their developed-market peers. The combination of our persistent cautious view on the dollar, attractive carry, improving credit quality and stronger fundamentals supports the case for maintaining exposure to the asset class.

Two forces continue to guide our portfolio construction. The first is artificial intelligence investment, which remains one of the most powerful drivers of earnings growth and equity-market leadership. The second is geopolitics and its impact on natural resources, which is no longer only a temporary source of volatility, but also a structural investment theme. The US-Iran conflict has highlighted the vulnerability of global energy markets and the strategic importance of energy security. As a result, we remain invested in equities, with a preference for the US market, technology and sectors related to electrification and energy security, as higher-for-longer oil prices are here to stay. We also maintain gold as a core geopolitical and US dollar hedge, supported by central-bank demand and its role in portfolios during periods of rising uncertainty.

The conversations that matter

If the conflict in the Middle East ends in the coming weeks, why won't the oil price (Brent crude) go back to USD 60–70/barrel?

Even if the Middle East conflict ends within weeks, Brent is unlikely to return to USD 60–70/bbl because physical oil markets normalise far more slowly than headlines. Disrupted flows, higher shipping and insurance costs, rerouting costs, damaged infrastructure, and delayed production restarts will continue to constrain supply. On top of this, strategic reserve refilling, commercial restocking, and precautionary hoarding for energy security reasons will support demand. At the same time, geopolitical risk premiums remain elevated, as threats to Gulf navigation persist. Seasonal demand is also strengthening, while non-Middle East disruptions, including Russian export and refining outages, continue to tighten global balances. With much of the oversupply buffer already consumed, prices are likely to remain structurally elevated.

If I missed the April equity rally, how else can I add risk to my portfolio?

Whilst awaiting an equity market correction, investors can look to EM debt as a higher-beta segment within fixed income; the sub-asset class is expected to deliver high-single-digit returns this year. Even with spreads on EM hard currency debt having recovered to below pre-war levels, the all-in yield remains attractive and provides a meaningful cushion for either spread widening or higher rates. Importantly, index-level EM spreads mask significant dispersion, as there are countries that benefit directly from higher oil prices and countries that are acutely vulnerable as importers. We are positioned to capture this dispersion rather than owning the index. This opportunity is even greater in both frontier and local currency bonds. A diversified approach that takes in hard-currency sovereign and corporate bonds, as well as local currency and frontier countries, currently brings a yield of 7.5% for an average rating of BB+ and duration of 5.5 years.

What could derail the artificial intelligence investment cycle?

The main risks to the current AI trade are limited monetisation and technological disruption. On monetisation, AI adoption is accelerating rapidly and has already progressed very quickly amongst consumers; uptake by firms, however, has been slower. We expect this to accelerate as more companies invest in AI to improve productivity, automate workflows, and reduce headcount needs. The technological risk would be another ‘DeepSeek moment’, particularly if open-source models, especially from China, prove capable of delivering performance close to frontier models from OpenAI, Anthropic, and Google, whilst requiring significantly less computing power. For now, however, frontier models continue to lead. Their ability to raise increasingly large amounts of capital should help them preserve this advantage by giving them access to greater cloud computing capacity.

Macroeconomics

Growth and inflation are trapped in a ‘no war, but no peace’ tunnel

Markets are volatile, reacting to daily geopolitical news, and the world economy is already facing a global surge in inflation. The longer the Strait of Hormuz remains closed, the more negative the impact on the global economy will be, and fears of potential demand destruction are rising.

Some fiscal support has been provided to mitigate the impact of oil prices on economic activity, but this remains limited. The major central banks are currently maintaining a wait-and-see approach, but this could change if oil and inflation enter an upward spiral.

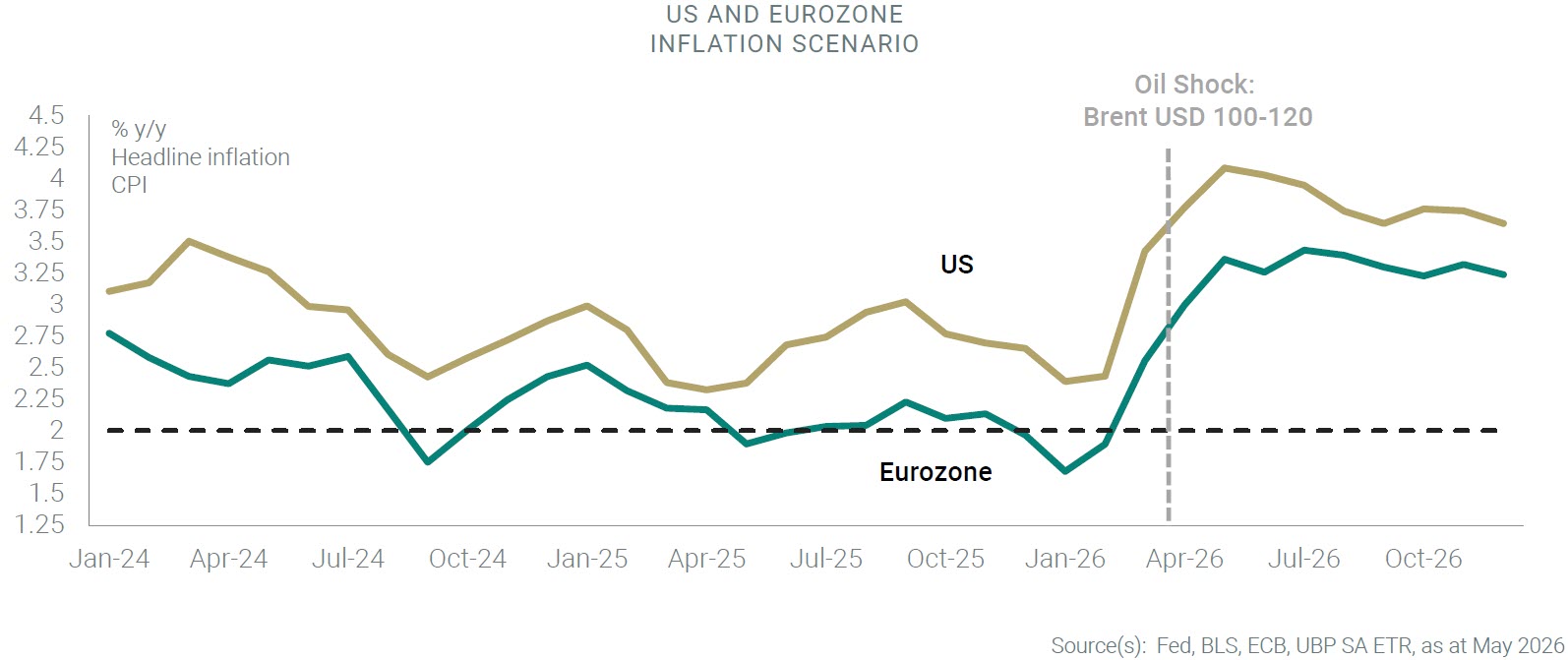

Following a resilient first quarter, the world economy is at a crossroads coming into Q2. Several scenarios are possible, depending on how the conflict in the Middle East unfolds, the level of geopolitical tensions, and the impact of the oil price shock on the economy. With Brent crude trading between USD 100 and USD 120/bbl, we expect to see higher inflation and slower growth, though not a recession. Some central banks could hike key rates this year, notably the European Central Bank (ECB), but the move in key rates should remain very limited at global level.

Conflict and the energy crisis: inflation picks up again

The conflict in Iran and the closure of the Strait of Hormuz have caused oil and gas prices to soar. Global inflation is picking up again and could reach around 4.0% in the coming months. This affects all countries, including the US: despite its status as an exporter of petroleum products, the price at the pump has risen by 25% over the past year. US inflation is therefore expected to approach 4.0% in the coming months, and is likely remaining between 3.5% and 4.0% in the third quarter.

In Europe, year-on-year inflation rebounded to 2.5% in March and is expected to rise to over 3.0% in the coming months. All eurozone countries are affected, but disparities will emerge as different national governments have implemented a range of measures to mitigate or cap energy price increases. In the UK, inflation is also expected to remain at around 4.0% in the coming months due to rising energy costs.

In Asia, China has emerged from deflation as energy prices have risen, with forecasts pointing to inflation of 2.5% in 2026. Similar pressures are being observed in Japan, India, South Korea and the Philippines. If higher energy prices continue to spread to other sectors, such as food and services, the rise in inflation could persist, which could lead to an inflationary spiral.

Growth wavers

Global growth showed resilience in the first quarter, as the Middle East conflict's impact on economic activity remained limited. However, its impact could become more apparent from the second quarter onwards, leading to a slowdown across various regions.

Europe and Asia are more vulnerable than China and the US because they are both net energy importers. Despite spending on infrastructure and defence, the growth outlook for Germany has been revised downwards to 0.6%. In Asia, some countries have implemented energy consumption restrictions, but semiconductor exports from Taiwan and South Korea have remained robust.

In light of the conflict, global growth is becoming increasingly fragmented but remains robust at 2.7%. US growth is expected to remain at around 2.0% thanks to investment in new technologies. Chinese growth could range from 4.5% to 5.0%, but consumption remains fragile amid the ongoing race for new technologies.

Monetary policy: central banks are worried about inflationary pressures

Central banks have adopted a more hawkish stance due to fears of a spiral of rising oil prices, inflation and wages. At their recent meetings, the Fed, the Bank of England (BoE) and the ECB showed patience, favouring a wait-and-see approach before making any decisions on key interest rates. However, given that inflation is expected to hover around 3%, the ECB is likely to raise rates in June. Meanwhile, there will be intense debate at the BoE over whether to prioritise weak growth or persistent inflation, and the Bank of Japan (BoJ) could continue its normalisation process in the coming quarter. Last, the Fed might cut rates in September, but this would require the conflict in the Middle East to be resolved swiftly, as the Federal Open Market Committee (FOMC) remains divided on inflation risks.

Some central banks in emerging markets have already raised interest rates, and this trend could continue depending on inflation prints in the coming months.

The conversations that matter

If the conflict in the Middle East ends in the coming weeks, why won't the oil price (Brent crude) go back to USD 60–70/barrel?

Even if the Middle East conflict ends within weeks, Brent is unlikely to return to USD 60–70/bbl because physical oil markets normalise far more slowly than headlines. Disrupted flows, higher shipping and insurance costs, rerouting costs, damaged infrastructure, and delayed production restarts will continue to constrain supply. On top of this, strategic reserve refilling, commercial restocking, and precautionary hoarding for energy security reasons will support demand. At the same time, geopolitical risk premiums remain elevated, as threats to Gulf navigation persist. Seasonal demand is also strengthening, while non-Middle East disruptions, including Russian export and refining outages, continue to tighten global balances. With much of the oversupply buffer already consumed, prices are likely to remain structurally elevated.

If I missed the April equity rally, how else can I add risk to my portfolio?

Whilst awaiting an equity market correction, investors can look to EM debt as a higher-beta segment within fixed income; the sub-asset class is expected to deliver high-single-digit returns this year. Even with spreads on EM hard currency debt having recovered to below pre-war levels, the all-in yield remains attractive and provides a meaningful cushion for either spread widening or higher rates. Importantly, index-level EM spreads mask significant dispersion, as there are countries that benefit directly from higher oil prices and countries that are acutely vulnerable as importers. We are positioned to capture this dispersion rather than owning the index. This opportunity is even greater in both frontier and local currency bonds. A diversified approach that takes in hard-currency sovereign and corporate bonds, as well as local currency and frontier countries, currently brings a yield of 7.5% for an average rating of BB+ and duration of 5.5 years.

What could derail the artificial intelligence investment cycle?

The main risks to the current AI trade are limited monetisation and technological disruption. On monetisation, AI adoption is accelerating rapidly and has already progressed very quickly amongst consumers; uptake by firms, however, has been slower. We expect this to accelerate as more companies invest in AI to improve productivity, automate workflows, and reduce headcount needs. The technological risk would be another ‘DeepSeek moment’, particularly if open-source models, especially from China, prove capable of delivering performance close to frontier models from OpenAI, Anthropic, and Google, whilst requiring significantly less computing power. For now, however, frontier models continue to lead. Their ability to raise increasingly large amounts of capital should help them preserve this advantage by giving them access to greater cloud computing capacity.

Macroeconomics

Growth and inflation are trapped in a ‘no war, but no peace’ tunnel

Markets are volatile, reacting to daily geopolitical news, and the world economy is already facing a global surge in inflation. The longer the Strait of Hormuz remains closed, the more negative the impact on the global economy will be, and fears of potential demand destruction are rising.

Some fiscal support has been provided to mitigate the impact of oil prices on economic activity, but this remains limited. The major central banks are currently maintaining a wait-and-see approach, but this could change if oil and inflation enter an upward spiral.

Following a resilient first quarter, the world economy is at a crossroads coming into Q2. Several scenarios are possible, depending on how the conflict in the Middle East unfolds, the level of geopolitical tensions, and the impact of the oil price shock on the economy. With Brent crude trading between USD 100 and USD 120/bbl, we expect to see higher inflation and slower growth, though not a recession. Some central banks could hike key rates this year, notably the European Central Bank (ECB), but the move in key rates should remain very limited at global level.

Conflict and the energy crisis: inflation picks up again

The conflict in Iran and the closure of the Strait of Hormuz have caused oil and gas prices to soar. Global inflation is picking up again and could reach around 4.0% in the coming months. This affects all countries, including the US: despite its status as an exporter of petroleum products, the price at the pump has risen by 25% over the past year. US inflation is therefore expected to approach 4.0% in the coming months, and is likely remaining between 3.5% and 4.0% in the third quarter.

In Europe, year-on-year inflation rebounded to 2.5% in March and is expected to rise to over 3.0% in the coming months. All eurozone countries are affected, but disparities will emerge as different national governments have implemented a range of measures to mitigate or cap energy price increases. In the UK, inflation is also expected to remain at around 4.0% in the coming months due to rising energy costs.

In Asia, China has emerged from deflation as energy prices have risen, with forecasts pointing to inflation of 2.5% in 2026. Similar pressures are being observed in Japan, India, South Korea and the Philippines. If higher energy prices continue to spread to other sectors, such as food and services, the rise in inflation could persist, which could lead to an inflationary spiral.

Growth wavers

Global growth showed resilience in the first quarter, as the Middle East conflict's impact on economic activity remained limited. However, its impact could become more apparent from the second quarter onwards, leading to a slowdown across various regions.

Europe and Asia are more vulnerable than China and the US because they are both net energy importers. Despite spending on infrastructure and defence, the growth outlook for Germany has been revised downwards to 0.6%. In Asia, some countries have implemented energy consumption restrictions, but semiconductor exports from Taiwan and South Korea have remained robust.

In light of the conflict, global growth is becoming increasingly fragmented but remains robust at 2.7%. US growth is expected to remain at around 2.0% thanks to investment in new technologies. Chinese growth could range from 4.5% to 5.0%, but consumption remains fragile amid the ongoing race for new technologies.

Monetary policy: central banks are worried about inflationary pressures

Central banks have adopted a more hawkish stance due to fears of a spiral of rising oil prices, inflation and wages. At their recent meetings, the Fed, the Bank of England (BoE) and the ECB showed patience, favouring a wait-and-see approach before making any decisions on key interest rates. However, given that inflation is expected to hover around 3%, the ECB is likely to raise rates in June. Meanwhile, there will be intense debate at the BoE over whether to prioritise weak growth or persistent inflation, and the Bank of Japan (BoJ) could continue its normalisation process in the coming quarter. Last, the Fed might cut rates in September, but this would require the conflict in the Middle East to be resolved swiftly, as the Federal Open Market Committee (FOMC) remains divided on inflation risks.

Some central banks in emerging markets have already raised interest rates, and this trend could continue depending on inflation prints in the coming months.

To download the full PDF, please contact your relationship manager or reach out to us via the form by clicking here.

The financial instruments and investment strategies portrayed in this document are for informative purposes only. They may differ from those effectively held in an investor’ portfolio. Depending on the jurisdiction and investment profile, one or some of these instruments and strategies – including, where applicable, options – may not be permitted, available or suitable. The opinions expressed herein are correct as at 11 May 2026 and are subject to change without notice. Any forecast, projection or target, where provided, is indicative only and is not guaranteed in any way.