Commercial agreements are fuelling market optimism, reinforcing confidence in a clear path for corporate earnings growth. As the earnings season progresses, 34% of S&P 500 constituents have published their results, with 80% surpassing analysts’ estimates. This week, attention will be focussed on key economic data and potential new trade agreements as the 1 August tariff truce deadline approaches.

Market recap

Beyond the numbers

Macroeconomics

Japan and the United States finalised a trade agreement, reducing reciprocal tariffs from 25% to 15%, and the European Union and the United States have also reached a deal. This agreement includes a 15% baseline tariff on most EU products (including cars), USD 750 billion of energy purchases from the US, USD 600 billion of investments in the US, and an unspecified level of purchases of US military equipment. Details of the deal remain limited, and a comprehensive assessment is still awaited, but the baseline tariff rate is to be lower than the 30% previously announced. Last, the European Central Bank (ECB) held rates steady, maintaining its cautious stance; we expect one more rate cut (to 1.75%) by year-end.

The Federal Open Market Committee (FOMC) is expected to follow suit this week, as Fed governors weigh the impact of tariffs on their dual mandate. While rates are likely to remain unchanged for now, we anticipate two cuts by year-end. In addition, the US Treasury will release its Q3 refinancing estimates, shedding light on its strategy for financing the growing budget deficit. In the coming days, key economic data will take centre stage; these include US Q2 25 GDP flash, US payrolls, EU July CPI and potential trade deals as the 1 August deadline looms.

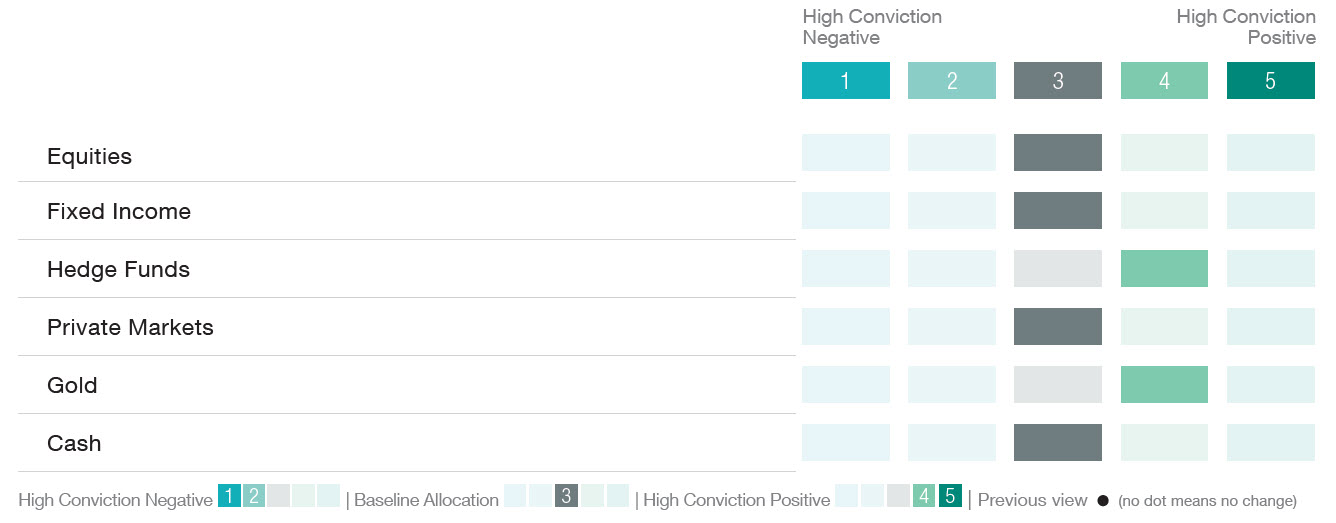

Asset allocation: strategic views as at July 2025

Equities

Global equities continued their upward march with the MSCI ACWI (total return) gaining +1.4%, buoyed by a risk-on mood driven by positive trade headlines between the US, Japan, and the EU. However, in a reversal from previous weeks, the global technology sector was among the laggards, posting a modest gain of just +0.3%. This was despite strong results from Alphabet which demonstrated solid demand for artificial intelligence (AI) and continued AI-related spending, as investors broadened their exposure to other areas of the market.

Despite the technology sector’s underperformance, major US indices still registered new all-time highs last week. Since our upgrade of US equities to a 4/5 conviction level (from 3/5 previously) at the start of July, they have outperformed global markets (S&P 500 +3.0% vs. global equities +2.6%), driven by the strength of the technology sector (S&P 500 Technology Index +4.5%, ‘Magnificent 7’ +4.1%).

The announcement of trade deals upheld growth projections and offered confidence to investors that the path for corporate earnings expansion remains clear. Furthermore, the Wall Street adage of ‘don’t short a dull market’ seemed particularly fitting, given the steady upward move by equities and persisting low levels of volatility over the week. This was further exemplified by the return of outsized movements in heavily shorted, so-called ‘meme’ stocks, as observed in the 2021 GameStop saga.

As of Friday, 34% of S&P 500 constituents had published results with an 80% beat rate. EPS growth for Q2 now stands at +6.4% vs. +4.9% expected at the end of June. The week ahead will see another large batch of quarterly reporting (33% of S&P 500 constituents, including four of the ‘Magnificent 7’), with market sentiment also set to be swayed by central bank newsflow (FOMC meeting) and trade developments.

Trade deals offer confidence about a clear path for corporate earnings growth

Fixed income

Yield curves flattened in the US and EU, with shorter-dated rates rising and longer-dated rates falling. Investment grade (IG), high yield (HY) and AT1 spreads narrowed, returning 0.2%, 0.3% and 0.6% for the week, respectively. AT1s are now up 1.3% in July and 6.2% year-to-date, driven by strong demand for higher-yielding credit (AT1s have been one of our convictions in fixed income this year).

In emerging markets (EM), we highlight Mexico, which has said it will launch a USD 10 billion P-Caps bond issuance to support Pemex (the largest EM HY issuer), using the proceeds to buy investment-grade bonds as collateral for Pemex’s repo loans. This is clearly positive for Pemex, with spreads approaching post-Covid-19 lows, prompting Fitch to place Pemex’s rating on positive watch. The off-balance-sheet structure avoids direct state guarantees, offering a novel approach to bolster Pemex without increasing Mexico’s debt.

AT1s are up 6.2% year-to- date, driven by strong demand

Forex & Commodities

Reflecting optimism on an EU–US trade agreement and better-than-expected eurozone composite PMI data, the EUR/USD rose to highs of around 1.1780. The USD/JPY fell to levels of around 146.50, following Japan’s upper house election, and the JPY benefitted from the US–Japan trade deal announcement, while markets moved to price in an October rate hike by the Bank of Japan (BoJ).

The main highlight over the coming week will be the US Federal Reserve meeting, where rates are expected to remain on hold at 4.50%. The USD is unlikely to benefit, given the possibility of a split FOMC vote, thus presenting upside risks for the EUR/USD. The BoJ will meet on Thursday and it is likely to keep rates on hold at 0.50%. The USD/JPY is unlikely to break out of its recent ranges.

The EUR/USD climbed to highs of around 1.17

The opinions expressed herein are correct as at 28 July 2025 and are subject to change without notice. This information should not be relied upon by the reader as research or investment advice regarding any particular fund, strategy or security. Past performance is not a guide to current or future results. Any forecast, projection or target, where provided, is indicative only and is not guaranteed in any way.