Despite Nvidia’s stronger-than-expected results and upbeat guidance, investor sentiment remained fragile. A mixture of fatigue and doubts about AI, shifting expectations for a potential Federal Reserve rate cut in December, and a rise in long-term Japanese yields fuelled sharp swings across equity markets. This week, investors will closely monitor the continuing Russia–Ukraine discussions for signs of an end to the conflict.

Market recap

Beyond the numbers

Macroeconomics

The PMI services remained positive in the US and the eurozone but declined in the UK; conversely, sentiment deteriorated in the PMI manufacturing in the first two regions but improved in the UK. The manufacturing sector remains fragile due to limited exports and unwanted inventories.

In the US, confidence returned to industry and the real estate sector, but household confidence remained low amid concerns about inflation and unemployment. The labour market remains mixed. Non-farm payrolls increased by 119,000 in September, but the unemployment rate rose to 4.4%.

In the eurozone, final inflation for October came in in line with the initial estimates (0.2% m/m; 2.1% y/y) but remained above 2.0% y/y due to the price of food and services. UK inflation has declined from 3.8% to 3.6% y/y thanks to lower energy and services costs.

The October FOMC minutes revealed that most Fed governors favoured keeping rates unchanged in December. The FOMC noted upside risks to inflation versus downside risks to activity and labour.

The new Takaichi government has announced a significant fiscal stimulus package worth USD 135.5 billion.

This week, the German Ifo and the European Commission confidence indices are expected to show a mixed picture. In the US, Q3 GDP is expected to be above 3.5%. In the UK, the Autumn budget will probably announce a mixture of spending cuts and potential tax hikes.

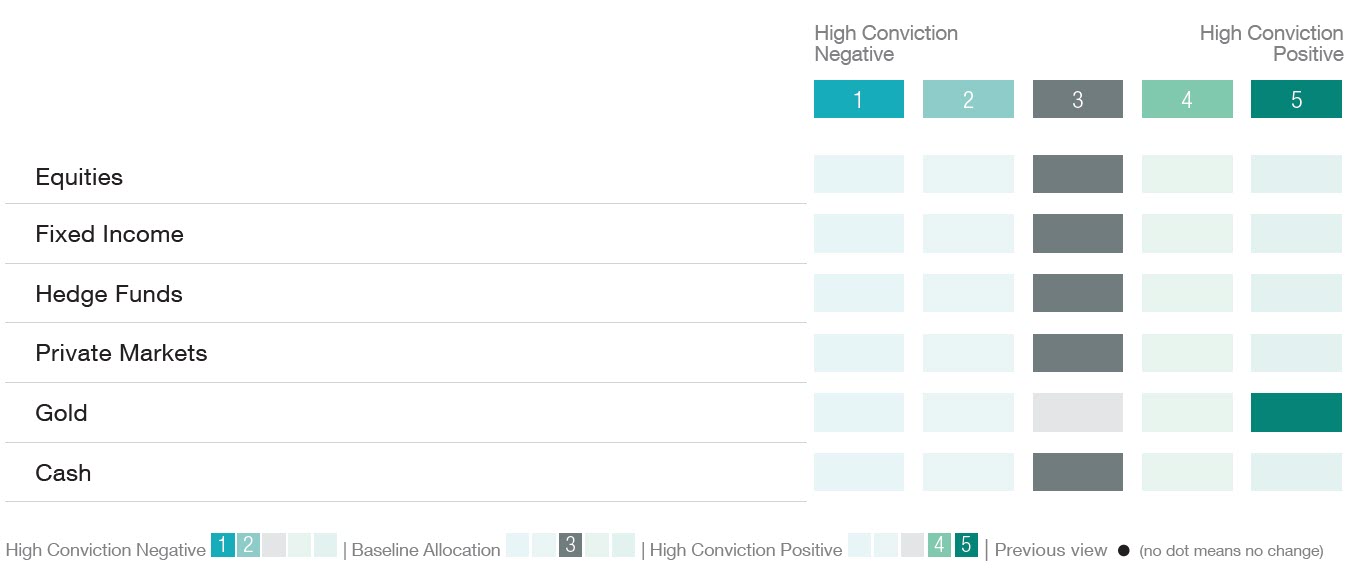

Asset allocation: strategic views as at November 2025

Equities

Global equities declined during a rollercoaster week (MSCI ACWI Total Return: -2.5%) as market sentiment was impacted by several factors: AI fatigue and monetisation concerns, fluctuations in expectations of a December Fed rate cut, and rising long-term Japanese yields which sparked fears of another unwinding of popular carry trades that would see Japanese investors liquidate overseas positions and repatriate investments domestically.

Despite better-than-expected results and upbeat guidance from Nvidia, investor jitters persisted. The global technology sector bore the brunt of the risk-off sentiment (-4.8%, Magnificent 7: -1.9%), while consumer staples and healthcare were the only sectors to finish the week in positive territory.

Strong year-to-date gains (global equities total return +17.4%) are prompting investors to focus on performance preservation ahead of the final Fed rate decision of the year. With market sensitivity to this decision running high, participants are hopeful it will serve as a clearing event and pave the way for a ‘Santa rally’ into year-end. Developments regarding an end to the Russia–Ukraine conflict will also be closely monitored as discussions between the two nations continue this week.

Strong year-to-date gains are prompting investors to focus on performance preservation

Fixed income

Performance for the safest segments of fixed income performed well, with Treasuries and investment grade (IG) returning 0.4% for the week, while the riskier segments (HY, AT1, EM) were all flat. The US 10-year continues to trade in a tight 4.00–4.15% range, with its yield narrowing by 10 bps to 4.05%, while IG and high-yield spreads moved up by 5 bps and 10 bps, respectively.

The implied probability of the Fed cutting in December swung significantly, starting the week at 40%, moving down to 25% by Wednesday and finishing the week at 65%. The swings come on the back of a combination of delayed US economic data releases that gave mixed signals on inflation and labour market health, as well as divergent Fed policymaker rhetoric, including the Dallas Fed president saying it would be ‘appropriate’ to hold rates steady in December unless there is further evidence of inflation declining faster than expected, or the labour market cooling more rapidly, while New York Fed President Williams indicated that he sees potential for rate cuts ‘in the near term’.

A report from Blackrock showed credit metrics continued to improve in Q3, with aggregate covenant defaults and interest coverage ratios both moving in the right direction. PIK activity held steady from Q2, and private credit covenant defaults actually declined, though dispersion across deals remains wide. Heading into Q4, the peak in public/market defaults appears to be behind us, supported by decent economic growth, easing debt-service burdens, and still-resilient corporate fundamentals.

In Switzerland, the SNB president stated last week that he is prepared to cut rates further into negative territory ‘if necessary’, as the strength of the Swiss franc remains a significant issue.

The implied probability of the Fed cutting rates in December swung significantly due to delayed US data releases

Forex & Commodities

Last week, the USD edged higher against most major G10 currencies, as risk aversion spread over markets. Overnight index swaps (OIS) moved to price in a 25-bp December rate cut with a 75% probability by the end of the week. FOMC Member John Williams noted his support for a December rate cut. The main event for the USD in the coming week will be the publication of PPI and ISM data. Overall, we expect that the EUR/USD will trade at the lower end of its recent range in the coming week.

The USD/JPY traded higher to levels of just under 158, and Bank of Japan and Ministry of Finance officials increased their verbal interventions in a bid to reduce JPY depreciation pressures. Thirty-year JGB yields rose to multi-decade highs in an increased sign of worries about fiscal easing, and the steepening of the 2–30 curve weighed on the JPY. We do not believe that an FX intervention is imminent, and a USD/JPY upside above 158/160 is likely to provoke a more serious policy response.

The CHF weakened against both the EUR and the USD last week, despite a lack of any apparent catalyst. Coming so soon after the signing of the US–Switzerland trade agreement, we suspect that the Swiss National Bank (SNB) might have intervened. We will know more once the SNB publishes its FX transaction data in January 2026. In the meantime, we anticipate that CHF will maintain a generally robust profile.

The GBP/USD edged lower against the USD, ahead of this week’s UK budget. Most of the budget details have been leaked well in advance of the event itself, meaning it is unlikely to provide many surprises. The GBP/USD is likely to trade at the lower end of recent ranges, as investors reduce growth forecasts and price in additional Bank of England easing potential. We will revise our GBP forecasts following the budget.

Last, gold traded within a tight range, and volatilities declined to levels below 19%. ETF inflows have slowed, which likely explains the inability of gold to sustain rallies above USD 4,100 per oz in recent weeks. We maintain a highly constructive stance on gold over the medium term, expecting levels of USD 4,600 per oz by Q4 2026.

Risk aversion supported the USD against most major G10 currencies

The opinions expressed herein are correct as at 24 November 2025 and are subject to change without notice. This information should not be relied upon by the reader as research or investment advice regarding any particular fund, strategy or security. Past performance is not a guide to current or future results. Any forecast, projection or target, where provided, is indicative only and is not guaranteed in any way.