Our hedge fund insights this quarter is an update on our previous report on how market volatility impacts systematic and now discretionary strategies in 2026.

Key Point

Our hedge fund insights this quarter is an update on our previous report on how market volatility impacts systematic and now discretionary strategies in 2026. After the lows in implied volatility at the end of 2025, the spike through March has generated a wide spread of returns across hedge fund strategies and managers, with differing approaches to risk management influencing the size of performance reversals in Q2.

Performance Review

The old adage - “Markets go up the stairs and down the elevator” - is a good description of the performance of the hedge fund industry over the first quarter. Performance for the hedge fund industry was very good for the first two months of the year as all strategies benefited from an environment of reasonable economic growth and fixed income markets reflecting a disinflationary environment as the US 10 year yield fell from 4.2% to 3.9% over the period. At the index level, this meant gains of +2.4% led by Equity Long/Short as represented by the HFRX indices.

Themes driving the gains were EM asset re-rating, European growth, short USD/long commodity currencies. These long momentum themes were upended with the Iranian conflict which created a VaR shock through inflation-sensitive asset classes such as government bonds and FX. This began with discretionary macro managers who were long bonds due to the disinflationary theme driven by rapid AI adoption and short US dollar. As managers cut risk and sought liquidity, crowded trades such as gold suffered and spreads began to widen in the front end of bond markets, which triggered losses among the relative value rates managers. Equity option protection did not provide cover as equities remained more resilient to investor concerns.

Equity and credit markets tied to corporate earnings demonstrated less sensitivity as investors found it more challenging to price in the impact of higher inflation into earnings forecasts. The impact on hedge fund strategies was pronounced with Global Macro strategies the hardest hit with a loss of -3.7% in March partially offsetting the gains made in January and February. Return expectations for the next 18 months remain unchanged, mostly in-line with long term averages.

Hedge Fund Insights: An Update on Volatility’s Impact on Hedge Funds

The question we asked in the 2025 year-end report was whether the subdued volatility would continue? Our answer was that from a purely statistical perspective this was unlikely as implied volatility reached the levels of the 2010s when central bank policy was stable and accommodative and could be sustained due to disinflationary pressures. In contrast, heading into 2026, fiscal policy had supremacy with monetary policy relegated to a liquidity support function, against the backdrop of elevated geopolitical risks. This suggested a fertile opportunity in 2026 to trade actively in markets which had been more muted in the second half of 2025.

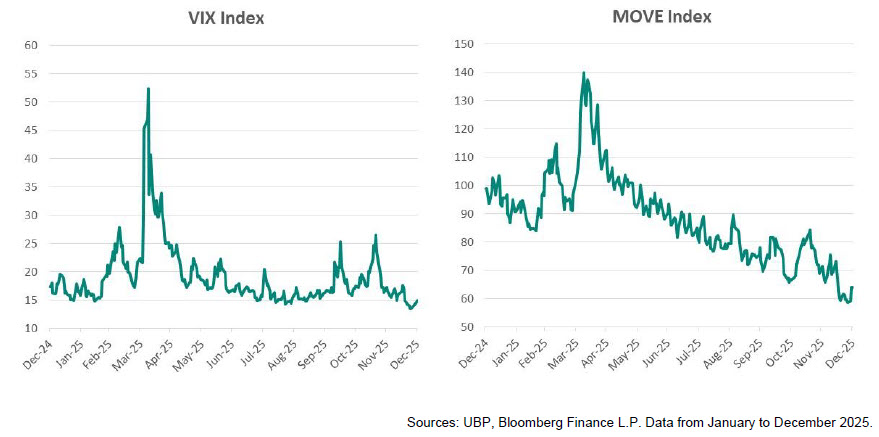

As the two charts below illustrate, from the lows of December 2025 implied volatility levels began to recover over the early part of the year. This accelerated in March, particularly in fixed income (MOVE Index), as geopolitical risks came to the fore and the sharp increase in oil prices impacted inflation expectations. Starting with systematic strategies, performance over January and February was broadly positive. Trend following outperformed as these strategies captured the rally in stocks and precious metals which both exhibited strong trend characteristics with volatility increasing but controlled. Short-term models saw opportunities across asset classes as increasing volatility improved the trading environment across both mean reversion and momentum sub-strategies. Fundamental driven strategies such as global macro continued their strong run from 2025 as long momentum and AI driven productivity themes led to a rally in bonds with expectations of lower inflationary pressure.

These themes were upended by the US/Israel attack on Iran which created a VaR shock across asset classes. For systematic strategies this meant risk reductions and cutting long equites, fixed income and short US dollar positioning, with shorter term models adjusting quicker. The sharp reversal was initially costly for trend following strategies but long exposure to Energy commodities provided varying degrees of positive offset. For the quarter, systematic strategies remained in positive territory.

In contrast, discretionary macro strategies generally saw a notable drawdown in March, which was mainly due to slower risk controls and a fundamental underpinning of trades. Even though managers trimmed risk initially, as the sell off continued, a combination of falling liquidity and higher correlations meant that as they wanted to exit, they were often met with even more challenging market conditions.

Figures 1 & 2: US equity and fixed income volatility in 2025 & 2026

Marketing communication. For Professional Investors in Switzerland or Professional Investors as defined by the relevant laws. Past performance is not a guide for current or futures results.

The views and opinions expressed by fund managers (internal or external) may differ from the house view. They are shared for informational purposes and do not constitute investment advice or a recommendation.