The last week of November ended strongly, following a period of market uncertainty. As December gets under way, seasonal patterns point to a firm year-end finish. However, attention is now turning to next week’s Federal Open Market Committee (FOMC) meeting. Market expectations became markedly more dovish in the final week of November amid growing concerns about the labour market; investors are now pricing in a 25-bp rate cut in December.

Market recap

Beyond the numbers

Macroeconomics

Market expectations for the Federal Reserve became decisively dovish during the last week of November. Recent comments from Fed officials have led investors to price a 25-bp rate cut in December, which aligns with our scenario.

This pivot reflects mounting concerns about the labour market: the ADP four-week cumulative measure shows job losses of around 54,000 through early November, consistent with the Fed’s Beige Book, which reported that employment had ‘declined slightly’. Adding to that, November consumer confidence deteriorated on both current conditions (index at 126.9 after 131.2 the previous month) and expectations (index at 63.2 after 71.8), as labour conditions are seen as being more difficult. Also, September retail sales disappointed, with the control group declining -0.1% over the month, but consumption should remain sustained in Q3 25.

Last, housing activity picked up modestly following a 75-bp fall in mortgage rates. Nevertheless, affordability remains a major challenge, with elevated mortgage rates compared with the pre-Covid-19 era.

In the eurozone, economic sentiment improved marginally in November, with the Economic Sentiment Indicator (ESI) rising to 97.6, but the recovery remains uneven: services continue to outperform (5.7 vs. 4.4 expected) while manufacturing lags behind (-9.3 vs. -8.3 expected). The eurozone November flash inflation print is due on Tuesday, but some country information was already released last week: inflation declined in France, Italy and Portugal, with significant declines in services price inflation, but it increased in Germany from 2.4% y/y to 2.6% y/y.

In the UK, the autumn budget outlined GBP 26 billion of tax increases by 2029–30, creating a larger-than-expected fiscal buffer. These measures are largely backloaded over the Office for Budget Responsibility’s five-year forecast window, which should limit the immediate hit to growth.

This week’s focus will be the delayed US September personal income and outlays report, which includes the core Personal Consumption Expenditures Price Index ( PCE) deflator. The markets will watch the ISM manufacturing index (expected to be 49.0) and the S&P Global Manufacturing PMI (51.9). Wednesday brings the ADP employment report alongside the ISM services index (52.0). In the eurozone, investors will monitor final manufacturing and services PMIs, the October unemployment rate, and final estimates for Q3 GDP.

Asset allocation: strategic views as at December 2025

Equities

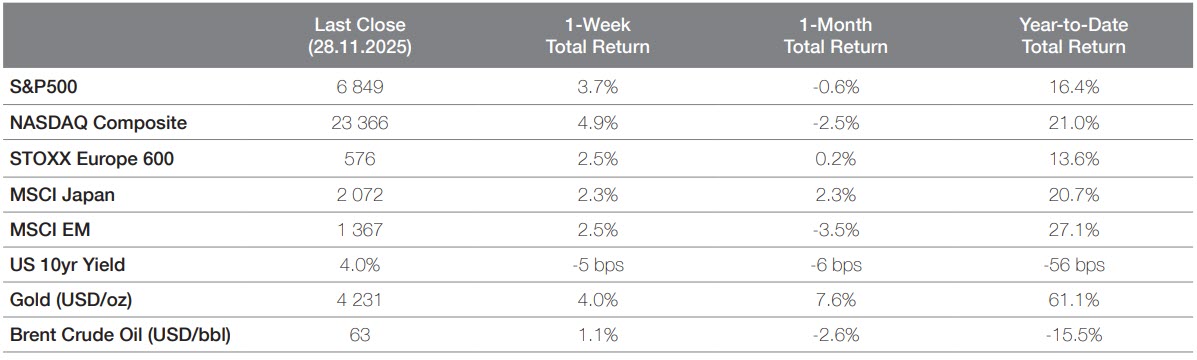

Global equities rebounded from the previous week’s decline (MSCI ACWI total return +3.6%), with US equities leading the recovery (S&P 500 +3.7%, Nasdaq +4.9%), held up by the Magnificent 7’s strength (+5.4%) and despite a holiday-shortened week.

Market optimism surged on growing expectations of a December rate cut by the Federal Reserve, with the probability now at 87%, compared with less than 40% at the start of last week. This shift was driven by several weaker-than-expected economic reports and dovish commentary from Fed officials. In response, investors moved up the risk curve, with cyclical sectors among the best-performing globally (materials +5.3%, consumer discretionary +4.4%), as well as US small caps (+5.5%).

Despite a few volatile weeks, global equities ended November with stable returns, while US equities managed to post modest gains (S&P 500 +0.3%). Seasonal trends suggest a strong finish to the year, as December has historically delivered an average gain of approximately +1.0% (S&P 500) over the past 30 years, with markets rising about 70% of the time.

Rising expectations of a December Federal Reserve rate cut provided fresh support to equity markets

Fixed income

Fixed income’s performance was positive last week, led by high-yield and AT1 segments (+0.5% each), while investment grade rose slightly less (+0.3%). Meanwhile, US 10-year notes experienced a positive trend, driven by increasing expectations of a December rate cut, with their yields narrowing by 6 bps to close to 4.00%.

The implied probability of a Fed cut in December now stands at 87% after rising materially over the week. On this note, Fed Governor Miran said that one of the causes of the deteriorating job market is the central bank’s policy setting target rates too high, and he is therefore calling for large interest rate cuts.

In the UK, debt investors reacted positively to the release of the latest budget by Chancellor of the Exchequer Rachel Reeves, as well as to the commitment of the UK government to reducing its debt, as the yields on 10-year gilts tightened by 10 bps during the week to roughly 4.45%.

In France, the political situation appears to have stabilised slightly over past couple of weeks, supported by less political noise and a decent set of economic data (inflation under control and resilient GDP growth in Q3). On this note, the yields on French 10-year OATs tightened by roughly 7 bps over the week to 3.40%.

UK debt investors reacted positively to the release of the new budget by the Chancellor

Forex & Commodities

Last week, the USD fell modestly against the majority of G10 currencies, as US consumer data looked slightly weaker. Consumer confidence data printed well below expectations, and the Fed’s Beige Book showed that low-income consumers are tightening their belts. The main event over the coming week will be the publication of US jobs data (ADP and Challenger). We expect that the USD should trade with a generally weak bias.

The GBP rose following the UK budget, and UK gilt yields declined, due to an expectation of increased fiscal buffers in the coming years. The budget’s plans to reduce household energy bills should lower inflation by around 0.3% next year, bringing it to levels of around 2.50%. This gives the Bank of England room to cut rates in the near term, and we anticipate that it will cut rates in December by 25 bps, taking its base rate to 3.75%. Overall, we do not expect the GBP to do a lot over the coming week, given the dearth of significant data releases.

The JPY rallied following the Governor of the Bank of Japan’s speech in which he gave his support for a December rate hike. OIS show an 80% probability that the Bank of Japan will raise deposit rates by 25 bps, taking them to 0.75%. We maintain a cautious stance on the JPY, and we believe that further aggressive JPY appreciation is unlikely in the near term.

Gold soared to levels of above USD 4,200 per oz, following the upward move in the silver price. Gold’s move is consistent with the price action we are seeing in real rate expectations, as proxied by ten-year TIPS yields. Silver’s upward move is interesting, because it reflects a breakout not only above recent ranges, but also in the gold–silver ratio. We note that the upward move is happening despite the lack of positive industrial demand, particularly from the PV sector in China.

The USD is expected to trade with a weak bias

The opinions expressed herein are correct as at 01 December 2025 and are subject to change without notice. This information should not be relied upon by the reader as research or investment advice regarding any particular fund, strategy or security. Past performance is not a guide to current or future results. Any forecast, projection or target, where provided, is indicative only and is not guaranteed in any way.