Chinese authorities are now fully behind the technology sector after years of cracking down on it. Self-sufficiency in semiconductors and AI has become a top strategic priority, driven by geopolitical tensions.

Global investors have sat up and taken notice, driving outperformance in the Hang Seng Tech (HSTECH) Index, which delivered +23% in 2025, the second consecutive year of strong positive performance after three years of negative returns (from 2021).

Sector has re-rated but not expensive

The HSTECH is now trading at 19.9x forward P/E, 11% below its five-year historical average of 22.5x. Global tech represented by the Nasdaq continues to trade at a 26% premium to the HSTECH. While this has narrowed from a peak of over 100% (in September 2024), it is interesting to note that, prior to 2023, the China tech sector had typically been more expensive, suggesting further room for valuation expansion.

AI innovation flourishing

China is the only meaningful global competitor to the US in the AI race, with the industry having seen rapid development since the launch of DeepSeek in early 2025.

US restrictions on chip access have forced China’s developers to innovate. Chinese AI models are high- quality, cost-efficient and open source. Technology companies can focus on building and monetising applications, supported by the advantage of a large domestic market.

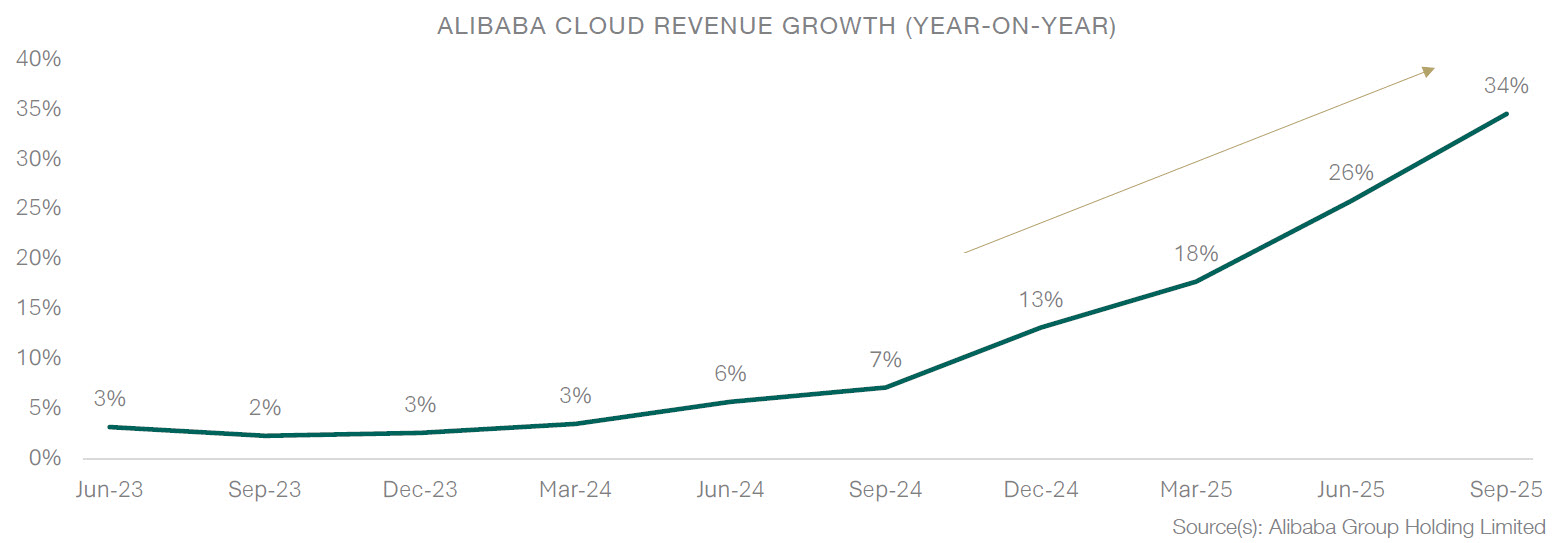

2026 is likely to bring accelerating AI infrastructure spending, product roll-outs, and a steep ramping up of monetisation (in both cloud computing and adtech).

Some uncertainties around earnings growth

Deflation, soft consumption and weakness in the real estate sector are issues that need to be resolved. China tech companies are mostly consumer facing, and 2025 earnings have been ravaged by intense competition in electric vehicles (EVs), food delivery, and quick commerce.

The consensus now expects -15% earnings per share (EPS) growth in 2025, followed by a 36% rebound in 2026 as competition subsides, although visibility remains low.

We maintain a baseline stance on the sector, but upside risks are emerging. The economy may soften further, but tech valuations are supportive, and AI is a strong driver.

Economic growth may bottom out as early as Q1 26, as the government has made boosting domestic consumption its top strategic priority in 2026. This would be a catalyst to add further exposure to the sector.

Read our Investment Outlook 2026 for more insights.

The financial instruments and investment strategies portrayed in this document are for informative purposes only. They may differ from those effectively held in an investor’ portfolio. Depending on the jurisdiction and investment profile, one or some of these instruments and strategies – including, where applicable, options – may not be permitted, available or suitable. The opinions expressed herein are correct as at 19 January 2026 and are subject to change without notice. Any forecast, projection or target, where provided, is indicative only and is not guaranteed in any way.

.jpg)