While President Trump is pressing for greater influence over the Fed in the pursuit of lower interest rates, US small caps continued to benefit from declining short-term US yields. Attention turned to Nvidia where strong Q2 earnings were eclipsed by underwhelming guidance and geopolitics impacting sales in China, sending the stock lower; even so, global technology equities outperformed. This week, the focus is set to shift to key US macro indicators, namely employment data.

Market recap

Beyond the numbers

Macroeconomics

US Q2 GDP has been revised upwards (from 3.0% to 3.3%) thanks to firmer investment and sustained domestic demand (1.9% q/q); otherwise, orders for capital goods (non-defence and excluding aircraft) were up by 1.1% in July. We maintain a view in favour of a soft-landing scenario on US growth in H2 25, in which investment is favoured by economic policy. US consumer confidence came in lower than the previous month, with falling expectations and rising inflation expectations. Core PCE was in line with the consensus, up by 2.9% y/y due to higher prices for both goods and services.

In Europe, IFO expectations remain on an upward trend and industrial confidence in the eurozone made some progress, whereas consumer confidence in the eurozone and Germany remained fragile. Data showed that Swiss GDP growth slowed down in Q2 (0.1% after 0.4% in Q1) due to a sharp decline in investment and a smaller contribution from trade.

The French prime minister has called for a vote of confidence on the budget (to be held on 8 September), with polls suggesting he will probably lose, opening the door to a renewed period of political and fiscal instability.

Noise on the US markets about the Fed’s independence continues, while the pressure on Fed Governor Cook has shifted to a legal fight after Trump fired her.

This week, the focus will be on final PMI and US employment data: after the negative surprise of large downward revisions to previous data and the shift in the Fed’s balance of risks, the labour surveys (ADP, JOLTS; non-farm payrolls and the unemployment rate) will be closely scrutinised. The consensus expects 75,000 jobs to have been created in August, up from 73,000 in July.

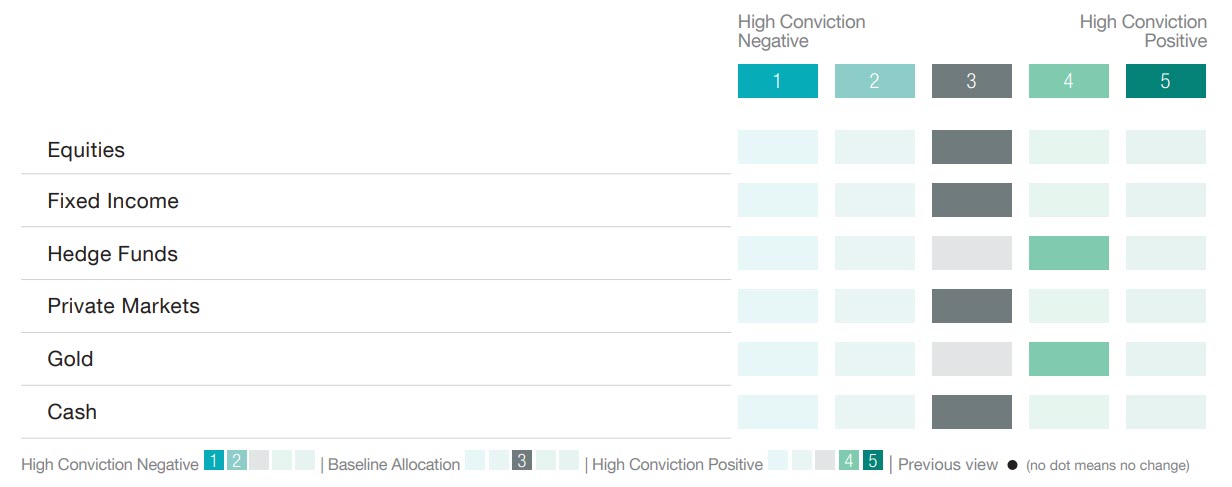

Asset allocation: strategic views as at September 2025

Equities

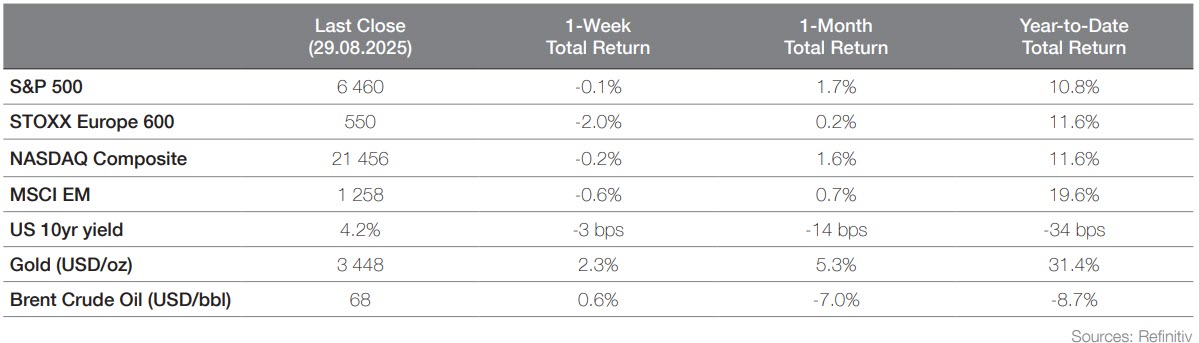

Global equities ended the week slightly lower (MSCI ACWI -0.4%), with US small caps (Russell 2000 +0.2%) outperforming for a third consecutive week, benefiting from declining short-term US yields and their exposure to variable-rate debt.

The S&P 500 (-0.1%) hit a record high before retreating on the back of inflation concerns, while European equities (STOXX Europe 600 -2.0%) lagged behind due to renewed tariff uncertainties, political instability in France, and fading hopes of a Russia–Ukraine ceasefire.

Investor attention focussed on Nvidia, whose strong Q2 earnings were overshadowed by underwhelming guidance and geopolitics impacting sales in China; this caused the company’s shares to decline over the week. Despite this, global technology stocks outperformed (+0.2%).

Looking ahead, US macroeconomic data will likely drive near-term market movements, with key indicators being released every day this week. Positive surprises could fuel continued sector and style rotation, a trend that has been observed over the past month.

Despite a decline for Nvidia, global technology stocks outperformed (+0.2%)

Fixed income

US Treasury yields continued their downward grind, with 2-year rates down 8 bps while 10-year rates were down 3 bps, and the 30-year edged up marginally; since the beginning of the year, 2-year rates are down 62 bps, 10-year down 34 bps, and 30-year up 15 bps. High yield (HY) spreads were flat while investment grade (IG) widened marginally; lower rates drove positive returns, with Treasuries, IG, and HY up 0.3%, 0.2%, and 0.4%, respectively, while emerging market and AT1s rose 0.1%.

The political crisis in France persists, pushing yields higher: French 10-year government bonds finished at 3.51%, exceeding Portuguese, Spanish, and Greek yields, and they are just 7 bps below Italian ones (for reference, they started this year 30 bps below Italian government bonds, and were 110 bps lower at the start of 2024). Naturally, French banks’ CoCos are under pressure, down around 1.1% so far; during the snap parliamentary elections of summer 2024, French CoCos fell by between 2% and 4%, taking about a month to recover. While we might see further volatility (Fitch is set to review France’s AA- rating on 12 September), bank fundamentals remain solid, and we continue to like the overall asset class despite tight valuations.

In the US, Trump fired Fed Governor Lisa Cook on 25 August, citing alleged mortgage fraud as cause (this included false statements on loan applications to secure lower rates and two mortgage applications two weeks apart, both of which were listed as primary residences). She sued to block it, arguing it violates the Fed’s independence. Federal Housing Finance Agency (FHFA) head Pulte escalated with a second criminal referral on 29 August, alleging that beyond the initial issues that had been flagged, Cook misrepresented a property in Cambridge, Massachusetts as a second home in 2021 for lower interest rates but listed it as a rental just months later. This underscores Trump's strategy for greater Fed control to achieve lower rates.

The persisting political crisis in France is pushing yields higher

Forex & Commodities

Last week, most currencies traded within recent tight ranges, with the USD having only limited reactions to threats to the Federal Reserve’s independence from the Trump administration. The EUR was largely unaffected by the prospect of a return to French political instability, which is consistent with price action since the eurozone sovereign debt crisis. The main event for the majors will be the publication of US NFP data on Friday. If the data print below expectations or we see another significant (negative) revision to previous data, it is likely to weigh on the USD. We will also get Swiss CPI data for August, which should show a rise of 0.2% y/y. Such data would illustrate that Switzerland should avoid a deflationary profile, thus benefitting CHF exchange rates.

Gold rose to levels of just below recent all-time highs (USD 3,500 per oz), reflecting the challenges to the Fed’s independence; this was further reflected in the steepening of the 30-year US Treasury yield curve. We maintain a constructive stance on gold and highlight its significant upside potential.

Gold’s all-time highs (USD 3,500 per oz) reflect the challenges to the Fed’s independence

The opinions expressed herein are correct as at 01 September 2025 and are subject to change without notice. This information should not be relied upon by the reader as research or investment advice regarding any particular fund, strategy or security. Past performance is not a guide to current or future results. Any forecast, projection or target, where provided, is indicative only and is not guaranteed in any way.