Doubts over a December interest rate cut by the Federal Reserve and concerns over the scale and timing of AI-related capex weighed on sentiment, underscoring the fragile market landscape. Now that the US government’s 43-day shutdown has ended, investors are awaiting the delayed September non-farm payrolls report this week. The publication of the minutes from the Federal Reserve’s meeting and Nvidia’s earning report, both on Wednesday, will be also closely scrutinised.

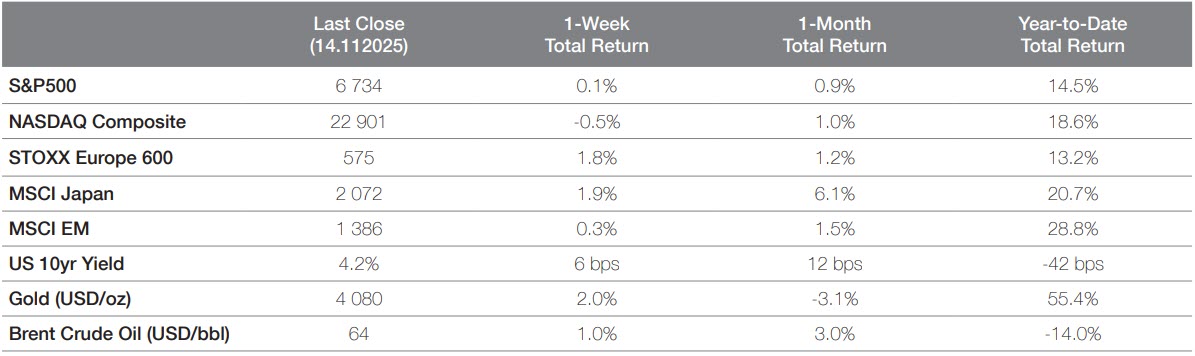

Market recap

Beyond the numbers

Macroeconomics

The US government shutdown ended after a record 43 days, with President Trump signing a funding bill passed by the House of Representatives to keep federal agencies operating until January 30. With the Bureau of Labor Statistics now reopened, a backlog of delayed economic data releases will be cleared in the coming weeks, beginning with the September non-farm payrolls report.

Private-sector indicators have therefore been centre stage. The October ADP report showed an average loss of 11,250 private-sector jobs per week through late October, reinforcing concerns about labour-market momentum. The NFIB small-business optimism index also fell to a six-month low of 98.2, with fewer firms planning to hire. Nevertheless, stable initial claims offer a measure of resilience.

Labour-market weakness was also evident in the UK, where unemployment rose to 5.0% in the three months to September, exceeding the Bank of England’s (BoE) 4.9% forecast. Payroll employment declined by 32,000 in October following a sharp downward revision for September. Combined with disappointing Q3 GDP growth, the data prompted markets to increase the probability of a BoE rate cut in December.

Across Europe, sentiment continued to deteriorate. Germany’s ZEW economic sentiment index fell to 38.5 in November, undershooting expectations of 41.0.

In parallel, Switzerland and the United States announced a new framework trade agreement under which US import tariffs on most Swiss goods would fall from 39% to 15%. In return, Swiss companies must invest USD 200 billion in the US by 2028 and Switzerland will reduce import duties on a range of US products.

In Asia, China’s economy showed renewed signs of cooling, with a sharp decline in investment and slower industrial output at the start of the fourth quarter.

This week, the markets will turn their attention to the rescheduled September non-farm payrolls report and the publication of the minutes from the Federal Reserve's meeting. Key economic data to watch include the Michigan consumer confidence index, potentially delayed monthly indicators, such as retail sales and industrial production, flash PMIs for Europe, Japan, and the UK, along with Japan's inflation figures and UK retail sales data.

Asset allocation: strategic views as at November 2025

Equities

Although global equities ended the week close to flat (MSCI ACWI +0.46%), price action was characterised by sharp swings and pronounced sector dispersion. The initial relief rally following the resolution of the US funding impasse faded quickly. Beneath the surface, leadership rotated: healthcare, energy and materials each gained more than 2%, while communication services and consumer discretionary stocks recorded weekly losses.

Volatility was driven in part by rising doubts over a December interest rate cut by the Federal Reserve. Several Fed officials adopted a hawkish tone, prompting markets to move from fully pricing in a quarter-point cut to assigning it a probability of only around 50%.

At the same time, concerns about the scale and timing of AI-related capex continued to weigh on sentiment, spilling over into equity market. Despite solid fundamentals, some of the most crowded AI beneficiaries saw further de-rating.

Overall, the week highlighted a fragile backdrop and reinforced the need for disciplined risk management into year-end.

Doubts over a US rate cut in December and concerns about AI-related capex are fuelling volatility

Fixed income

Rates were broadly higher during the week (+4–5 bps) in both the US and Europe, while spreads remained largely unchanged, leading to broadly flat performance at sub-class level (Treasuries and investment grade -0.1%, high yield, AT1s and emerging market +0.1%).

The Trump administration floated the idea of federally backing 50-year mortgages to address housing affordability. This would require regulatory changes, such as amending the Dodd-Frank Act but would likely have wide political backing. The monthly payment on a USD 500,000 mortgage would decline by USD 350 (assuming similar rates to 30-year terms), while obviously significantly increasing the lifetime interest cost of the mortgage. However, the monthly savings would be substantial and likely spark life back into the housing market, which has been very slow given high interest rates and affordability problems; this would then provide another boost to the economy.

There was significant volatility around UK rates. Earlier in the week, UK 2-year gilt yields dropped to their lowest levels in over a year following the publication of weak labour data. On Friday, yields spiked on reports that the UK’s Chancellor of the Exchequer, Rachel Reeves, had abandoned plans to raise income tax thresholds in the upcoming budget. Markets interpreted this as increasing the UK’s fiscal deficit, thus pushing yields higher, with rumours over the weekend indicating that Reeves is planning a new levy on high-value homes to raise around GBP 600 million. We will get more clarity on 26 November, when the UK’s budget is unveiled.

UK 2-year gilt yields dropped to their lowest level in over a year following the publication of weak labour data

Forex & Commodities

Last week, risk aversion crept into the FX markets, resulting in a pronounced outperformance for the CHF. The EUR/CHF fell to below 0.92, and the USD/CHF fell to levels of 0.7950. The USD did not benefit to any extent from the end of the US government shutdown, and we note that several Fed speakers placed significant weight on the US’s inflation outlook. Overnight index swaps (OIS) moved to price in a December rate cut with a 45% probability, down from 60% earlier in the week. The coming week has two main event risks for the USD, with the publication of the FOMC minutes from its last meeting and PMI data, which will be released towards the end of the week. Overall, we expect that recent ranges will hold for the main USD crosses.

The GBP weakened across the board following reports that the UK’s Chancellor of the Exchequer would not raise income tax in the forthcoming budget, leading to questions about the competence of the Labour administration. UK gilts also underperformed. The main risk event for the GBP this week will be the publication of UK CPI data for October, which are expected to print at 3.50% y/y. Headline risks will remain elevated in the coming days, and we prefer to express GBP shorts against the EUR.

The JPY weakened, and we note that officials at Japan’s Ministry of Finance increased their verbal interventions. We do not believe that any forex interventions will occur in the near term, and this gives continued scope for a USD/JPY upward move to levels of above 155/156 in the near term, which is above our December forecast. The main event risk for the JPY will be the publication of national CPI data; we do not anticipate that these will be market-moving. Overall, we have no reason to expect the yen to materially appreciate in the near term.

Gold saw large moves over the week, falling to lows of around USD 4,050 per oz in late trading on Friday as markets moved to reduce expectations of a Fed rate cut. Silver also suffered significant volatility, trading in a 12% range over the week. We continue to favour gold over the medium term.

Despite the pull-back, we continue to favour gold in the medium term

The opinions expressed herein are correct as at 17 November 2025 and are subject to change without notice. This information should not be relied upon by the reader as research or investment advice regarding any particular fund, strategy or security. Past performance is not a guide to current or future results. Any forecast, projection or target, where provided, is indicative only and is not guaranteed in any way.