The latest US inflation data confirm that price pressures are set to trend higher in the coming months. Nevertheless, rate cuts remain on the table given the slowdown in the labour market. As earnings season winds down after a solid set of results, market attention will shift to GDP developments and leading indicators, as well as to the Fed’s annual Jackson Hole meeting on Friday.

Market recap

Beyond the numbers

Macroeconomics

The US July CPI was in line with expectations (0.2% m/m; 2.7% y/y), showing a limited impact of tariffs on prices and fuelling expectations of a Fed rate cut in September. Nevertheless, core inflation reached 3.1% y/y, with prices for transportation, medical services, and personal services resuming their upward trend. The US PPI also confirmed rising inflationary pressures, with the index exceeding forecasts at 0.9% m/m and reaching 3.3% y/y. Retail sales for July were strong, but consumer confidence fell in August amid rising inflation and concerns about employment.

These data confirm our scenario of a gradual recovery in inflation over the next few quarters. Nevertheless, our scenario maintains its forecast of two rate cuts in H2 25, beginning in September, given the weakening labour market and slower domestic demand. Pressure from the White House and the US Treasury on the Fed to significantly reduce rates has intensified, but Fed governors generally remain cautious.

UK GDP growth was more resilient than expected in Q2 25, rising by 0.3% after 0.7% in Q1 thanks to high public spending, while private sector demand weakened. Meanwhile, the UK labour market continued to weaken, and wage growth slowed further to 4.6% year-on-year.

In Japan, Q2 GDP data were also better than expected: up by 1% q/q (annualised) thanks to robust investment and a positive net trade contribution; this will argue in favour of further adjustments to the Bank of Japan’s (BoJ) key rates in H2 25.

In trade news, the tariff truce between the US and China was extended for another 90 days. Overall, Chinese activity remained weak according to the July data, with modest growth in sales and property investment continuing to contract. This validates our cautious scenario of slow Chinese growth in H2 25.

The meeting between Trump and Putin regarding the war in Ukraine generated media excitement. However, Trump downplayed the likelihood of a peaceful resolution, while both Europe and Zelenskyy refuse to concede territory to Russia; European and Ukrainian leaders will meet Trump in Washington this week.

This week, the focus will be on UK CPI, which will probably continue to head towards 4% y/y, and retail sales. Flash PMIs in developed countries could remain weak; several central bank meetings in emerging countries are scheduled and the Fed will hold its traditional annual Jackson Hole meeting.

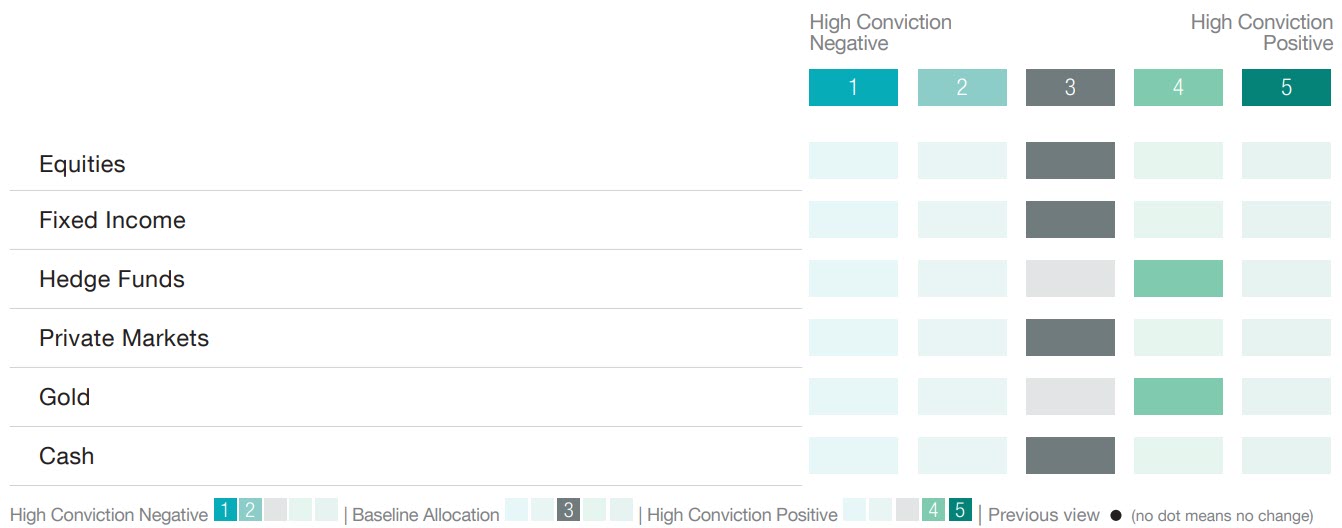

Asset allocation: strategic views as at August 2025

Equities

Global equities continued their upward march last week (MSCI ACWI total return +1.3%), with major US indices registering fresh all-time highs. Initial investor enthusiasm on July US consumer prices climbing no more than feared despite Trump’s tariffs was somewhat tempered by higher-than-expected producer prices. Nevertheless, market expectations for a rate cut in September remained elevated with an 85% probability of a 25-bp cut (CME FedWatch Tool), compared with 55% a month ago. Commentary from the US Treasury Secretary, who called for a 50-bp cut, further underpinned the risk-on sentiment observed over the week even though he later walked back his statements.

This led rate-sensitive and cyclical areas of the market to outperform (US small caps (Russell 2000) +3.1% vs. S&P 500 +1.0%), while traditionally defensive areas lagged behind the most: global consumer staples lost -0.2%, utilities were up +0.1%, and real estate gained +0.4%. Recent technology sector strength also took a backseat (-0.1% last week) following a strong outperformance since the start of July (+6.1% vs. global equities +3.9%) as investors moved up the risk curve and down the quality curve.

As of mid-August, more than 90% of S&P 500 constituents had published earnings with an 81% beat rate. As expected, US earnings growth for Q2 is settling well above consensus estimates at +11.8% vs. the +4.9% expected at the end of June. This has been supported once again by the technology sector (33.6% of the US benchmark index), which delivered +21.3% EPS growth vs. the +16.4% expected. The ‘Magnificent 7’ (34.1% of the index) have also been notable contributors, with an average Q2 earnings growth of +25.9% (excluding Tesla and Nvidia who will report at the end of August) vs. the +10.5% expected. This has led the M7 to strongly outperform markets over the past month (+6.8% vs. global equities +3.5%).

Europe’s report card came in with less satisfactory results, with Q2 earnings growth of +5.0%. Unlike in the US, the net earnings revision ratio is negative in Europe, particularly for eurozone companies. This is partially explained by a stronger euro, but a weaker economic growth backdrop and limited exposure to the technology sector (6.4% of the STOXX Europe 600 index) is leading to full-year EPS growth estimates of just +1.0% vs. +10.3% for the S&P 500. This has been reflected in the region’s underperformance over the past month (STOXX Europe 600 +2.4% vs. S&P 500 +3.1%, global equities +3.5%).

With the earnings season coming to a close, macro data is likely to dictate market fluctuations in the very near term as investors debate the path forward for interest rates and the US economy as the impacts of tariffs begin to be felt. For now, a ‘buy-the-dip’ mentality is offsetting the seasonally weak period that August and September have historically been for the S&P 500 over the past thirty years.

US earnings growth for Q2 is settling well above consensus

Fixed income

Fixed income markets performed well, helped by a slight spread compression. Treasuries were flat, whereas investment grade (IG) and high yield (HY) both gained 0.2%, and AT1s were up 0.4%; year-to-date gains stand at 5.3%, 5.5% and 7.5%, respectively. Duration-heavy EM outperformed (+0.6%), bringing year-to-date returns to 8.5%. In the eurozone, curves steepened as yields on maturities beyond 5 years increased, leading to slightly negative returns on government bonds and flat returns on both IG and HY.

Fed-related noise intensified, with Trump appointing the Chairman of the White House Council of Economic Advisors, Stephen Miran, as a replacement for Adriana Kugler who had resigned in early August. The FOMC board is now split between Trump and Biden appointees, with Miran being an advocate of tariffs and low rates. Trump is also narrowing down his picks for Chairman Powell’s replacement in 2026, with Kevin Warsh, Kevin Hassett, and David Zervos as top contenders, raising concerns about the Fed’s independence. Despite last week’s sticky PPI inflation data, Miran’s appointment and the potential announcement of new Fed Chair fuelled rate-cut speculation, contributing to bond yield volatility.

With markets currently assigning an 85% probability of a rate cut in September, and President Trump’s relentless pressure on the Fed to cut rates, all eyes will be on the Jackson Hole Economic Policy Symposium and Chairman Powell’s speech on Friday for further clues. As a reminder, last year, Powell signalled a pivot, saying that ‘[the] time has come for policy to adjust’ and that ‘my confidence has grown that inflation is on a sustainable path back to 2%’, eventually leading to the 50-bp cut in September.

Markets are currently assigning an 85% probability to a rate cut in September

Forex & Commodities

Last week, the USD weakened modestly (the US Dollar Index (DXY) fell by around 1%). US Treasury Secretary Scott Bessent called for a rapid front-loaded Fed rate-cutting cycle. Bessent noted a preference for rate cuts of around 175 bps, which would substantially reduce the USD’s nominal and real rate advantage, which would in turn weigh on the USD in the medium term. The main events for the USD over the coming week will be the publication of FOMC minutes from its last meeting and preliminary PMI data for August.

UK unemployment data printed in line with expectations, and the number of payrolled employees fell by less than expected. The data suggest that the labour market is not weakening as quickly as feared, pointing to a cautious Bank of England (BoE) easing cycle, and a less bearish GBP outlook. The main event for the GBP will be the publication of PMI data; a better-than-expected print will support a modest GBP/USD upside.

The Reserve Bank of Australia (RBA) cut rates by 25 bps, taking its base rate to 3.60%. Markets expect further rate cuts of around 50 bps. The AUD/USD rose to highs of around 0.6550. We expect further upside as the USD continues to weaken over time.

A better-than-expected print will support a modest GBP/USD upside

The opinions expressed herein are correct as at 18 August 2025 and are subject to change without notice. This information should not be relied upon by the reader as research or investment advice regarding any particular fund, strategy or security. Past performance is not a guide to current or future results. Any forecast, projection or target, where provided, is indicative only and is not guaranteed in any way.