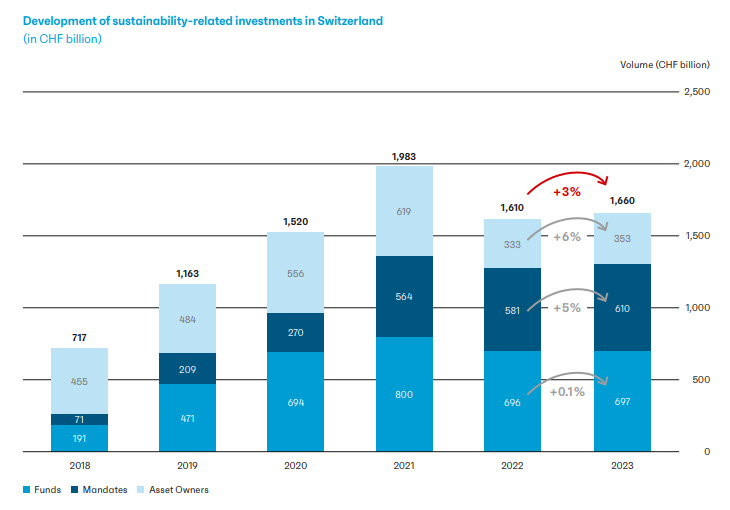

Sustainability-related investments in Switzerland returned to a growth path last year after seeing a significant drop between 2021 and 2022.

According to the Swiss Sustainable Finance (SSF) Market Study 2024, sustainability-related investments rose by 3% between 2022 and 2023, from CHF 1,610 billion to CHF 1,660 billion.

Many market participants have refined their methods to measure sustainability-related investments and no longer report investments that only use exclusions or ESG integration as a sustainable investment approach, which can explain why the growth was modest.

Our experts also believe that a number of external factors have shaped the recent developments of sustainability-related finance volumes.

In the wake of a period of overenthusiasm driven by political impetus, the Covid-19 pandemic and confidence in pure-play strategies, sustainable finance suffered a setback due to the emergence of complex regulations, geopolitical turmoil and a return to normal lifestyles. However, we are confident that with growing clarity and sophistication around sustainable investments, we will soon be on a more realistic growth path.

Nicolas Barben, Global Head of ESG Solutions

UBP is proud to feature among the report’s sponsors. As in previous years, we also responded to the survey alongside more than 80 financial market players, which served as the basis for the report.

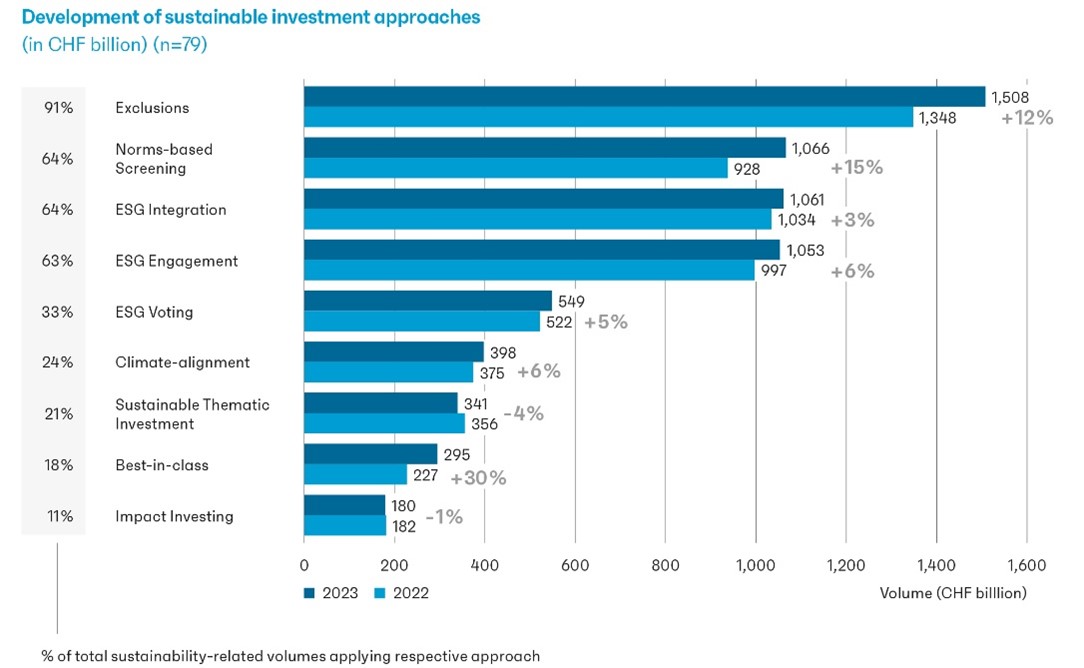

A tighter definition of “sustainability”

The study reveals that the maturity of sustainable investment approaches has increased, most likely spurred by the discussions about when the term "sustainable investments" is justified.

This year's results show that market participants have responded to the ongoing – sometimes controversial – discussions about the definition of sustainable investments and have, overall, increased the number of sustainable investment approaches applied.

Sabine Döbeli, CEO of SSF

Indeed, most sustainability-related approaches grew at or above the overall 3% increase in 2023, showing a trend towards using more combinations of approaches.

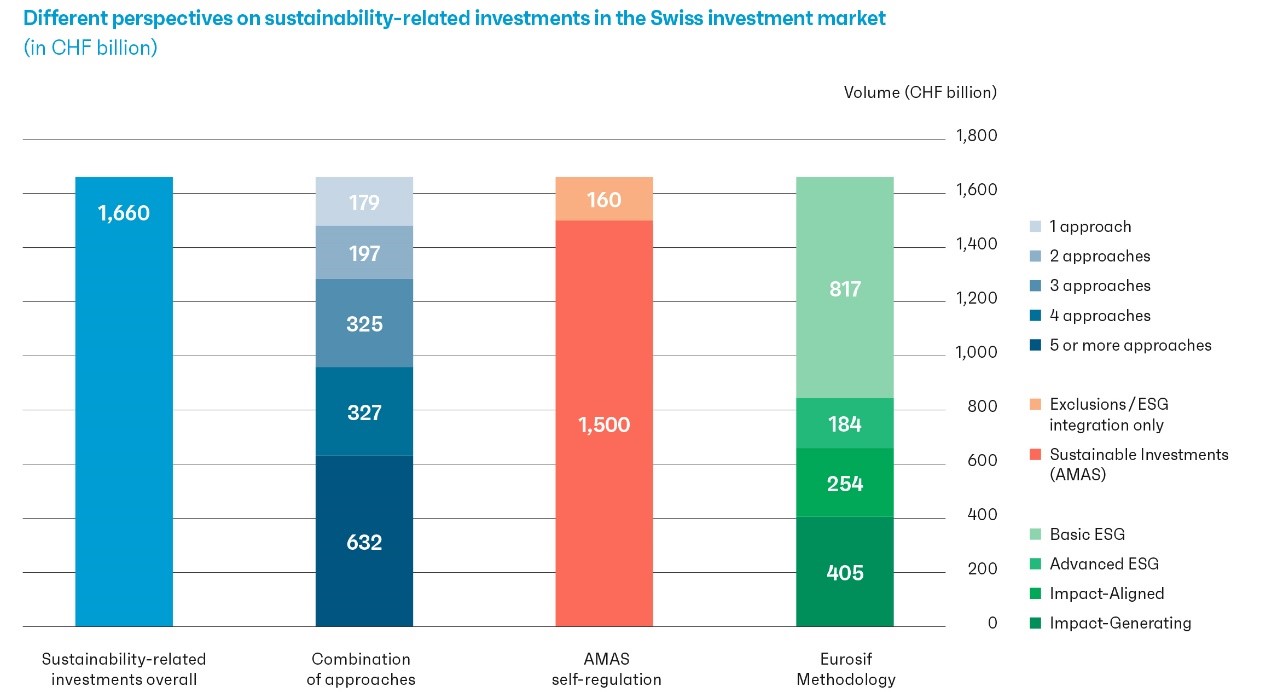

While the Swiss regulatory landscape remains fragmented and does not offer binding sustainability-related regulatory provisions that apply to institutions and products in all areas of the financial sector, EU regulations are constantly evolving as part of the bloc’s package of measures to develop a green economy and to set international standards.

This, together with voluntary initiatives, has led to a tighter application of the term “sustainable” by Swiss market players.

For example, the definition of the Asset Management Association Switzerland (AMAS) excludes volumes using only exclusion or ESG integration, and the share of investments applying this definition rose to 90% from 86% last year.

The study also looked at the methodology of the European Sustainable Investment Forum (Eurosif) which breaks down investments by ambition levels from basic ESG to impact-generating. It found a high level of impact-generating investments, mostly driven by effective engagement strategies.

Asset class distribution for sustainability-related investments

As in previous years, sustainability-related investments remain relevant across all asset classes, with equities, corporate bonds, sovereign bonds, and real estate continuing to lead. Together, these four asset classes account for around 77% of the total volume.

The full report as well as an Executive Summary in French and German are available on SSF’s website.