A clear light at the end of the coronavirus tunnel is now visible with the start of vaccination campaigns.

As a result, we see prospects for a brighter and safer economic environment for H2-21 and expect global economic growth to rebound strongly in 2021 (+5.0–6.0%) after a sharp decline in 2020 (-3.3%). While growth should be observed in all countries, we see additional upside potential in the United States with a unified government (Democratic presidency and Congress) paving the way for additional fiscal stimulus.

Key messages

- Economies have seen a gradual upturn in growth since summer 2020, but the resurgence of Covid-19 cases and a slower-than-expected start to the vaccination process are delaying the recovery.

- Nevertheless, we see prospects for a brighter and safer economic environment for H2-21, with global growth – led by China, Germany and the US – set to rise to 5.0–6.0% in 2021, after declining by 3.3% in 2020.

- Progress on the political landscape should also support the global economic recovery, notably in the United States, where the Democrats have secured a unified government (presidency and Congress), which paves the way for additional fiscal stimulus and accelerated economic growth.

Economies have seen a gradual upturn in growth since the summer of 2020, but the resurgence of Covid-19 cases (second wave, new variants) and the resultant new local restrictions, combined with a slower-than-expected vaccination process (particularly in Europe) are hampering the recovery as we begin 2021.

While we believe that available vaccines should prevent a third wave of the pandemic, they will not be able to stop the current wave. As a result, economic uncertainties will remain in place in Q1 but we feel a more constructive situation should emerge in Q2. Herd immunity through vaccinations in developed markets is expected to be reached in Q4, which will ease pressure on hospitals and allow a reintroduction of social mobility. We therefore see prospects for a brighter and safer economic environment in the second half of the year.

After registering a 3.3% decline in 2020, global economic growth should rebound sharply in 2021 (+5.0–6.0%), led by China (+8.0–9.0%), Germany (+4.0–5.0%) and the United States (+4.5–6.0%). We note that business sentiment in manufacturing remained resilient in January, fuelled by positive global demand, while orders and future production indicators moderated slightly from the previous month but remained well above their 2019–2020 levels.

The global economic recovery in 2021 should also be supported by the progress recently observed on the global political landscape.

In Europe, the vote in favour of the recovery fund (amounting to EUR 750 billion, or 5% of European GDP) will result in effective support for struggling countries and industries. The final UK–EU agreement on trade has avoided the risks of a no-deal Brexit and the associated WTO tariffs on trade. In China, the medium-term economic development targets will clarify the country’s new policy direction in 2021.

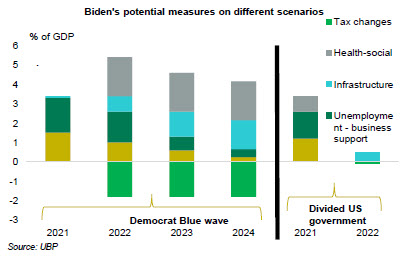

The Democrats’ taking control of the US Senate has resulted in a major shift in the balance of power in the United States (a unified government with the presidency and a narrow majority in Congress) and could change the shape of the US economy in the months ahead by accelerating the rebound that will likely come as more citizens are vaccinated (the target being 100 million people in the first 100 days of Biden’s presidency).

President Biden’s recently proposed USD 1.9 trillion economic rescue plan is also expected to help the US economy get back on track; this includes direct payments to Americans (USD 1400/person, up from USD 600/person), increased unemployment benefits, aid for state and local governments (USD 350 billion), more funding for the coronavirus pandemic response (USD 70 billion) and an increase in the minimum wage (to USD 15/hour).

The “American Rescue Plan” marks the first step in Biden’s response to the pandemic-induced economic downturn, with additional recovery measures reported to be put forward as early as February 2021 (according to the Financial Times). The second stage of Biden’s economic agenda is expected to call for increased longer-term spending on infrastructure, green energy and education, to be partially funded by higher corporate and individual taxes.

The US Senate vote on the rescue plan will not only be key to US economic recovery prospects in the shorter term, but also provides investors with an indication of Biden’s ability to convince Republicans to vote with the new administration.

Note: The products or services mentioned are provided as general information only and are not intended to provide investment or other advice. Not all products or services described are available in all jurisdictions. Past performance is not a guarantee of future results. For the full disclaimer, please refer to Legal Aspects.

Patrice Gautry

Chief Economist

Go to his Linkedin profile.

Alexandre Phily

Equity Specialist

Go to his Linkedin profile.