The fresh salvo of tariffs paused the rally on global equity markets, leaving them broadly stable. Renewed tariff threats are reigniting concerns about global industrial supply chains, generating doubts about whether or not these pressures will erode corporate margins. The upcoming earnings season, which kicks off this week, may offer some hints of an answer.

Market recap

Beyond the numbers

Macroeconomics

With trade agreements still limited ahead of the 9 July negotiating deadline, President Trump has extended the end date to 1 August. He issued new reciprocal tariffs on several emerging countries (Brazil is facing a 50% hike, for example), increased copper tariffs to 50%, and reiterated threats of 200% tariffs on pharmaceuticals. These announcements have revived the risk of a trade war and disruption of the industrial supply chain, which would result in higher costs for US consumers and manufacturers.

The publication of the minutes from the Fed’s June meeting revealed concerns about the impact of tariffs on inflation, as well as a split among governors regarding rate policy. Notably, there was little appetite for a rapid easing of key rates.

Next week, we will focus on inflation and retail sales in the US to assess the impact of tariffs on final prices and consumer resilience. Chinese economic data, particularly second-quarter GDP, should show relatively strong growth, despite uncertainties regarding trade and housing.

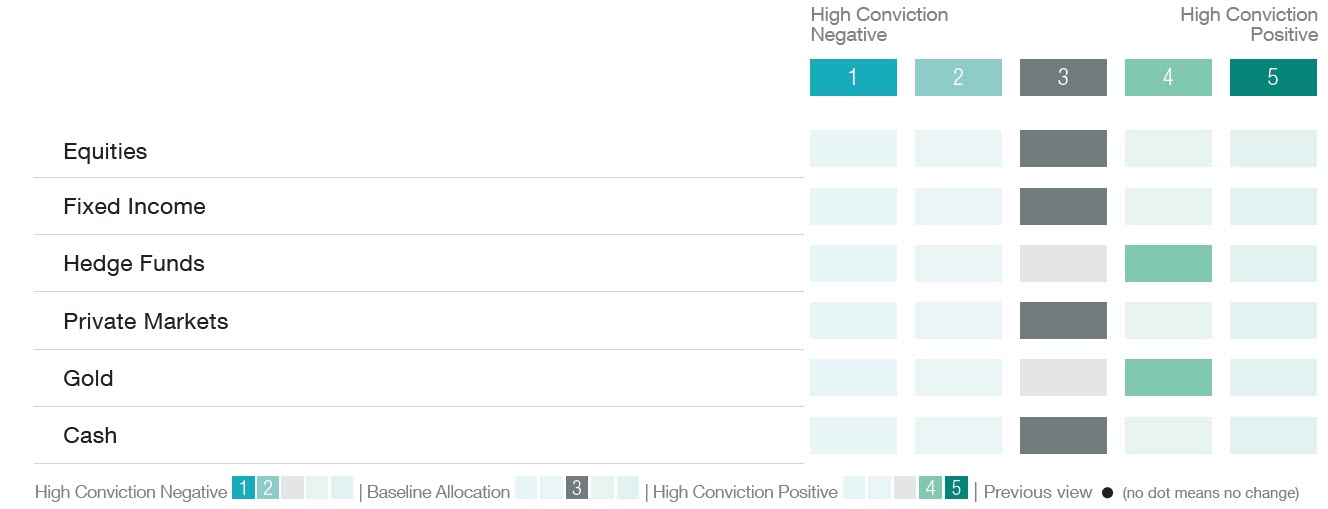

Asset allocation: strategic views as at July 2025

Equities

Global equities finished modestly lower last week, with the MSCI ACWI total return down by -0.3% as trade tensions re-emerged and dampened recent investor enthusiasm. Some appetite for European equities returned, with the STOXX Europe 600 up by +1.2% on hopes of a US trade deal, while US markets paused after three consecutive weeks of gains (S&P 500 -0.3%).

The previous week’s style rotation – with US small and mid-caps outperforming at the expense of larger-cap ‘quality’ and ‘growth’ names – failed to continue amid very choppy trading, with the Magnificent 7, once again taking the lead (+0.6% last week vs. US small and mid-caps’ -0.6%). This performance was driven in part by Nvidia surpassing the USD 4 trillion market capitalisation mark, the first company to achieve this milestone. This helped support the global technology sector, which remained stable over the week, while most other sectors finished the week in negative territory.

While successful US debt auctions midweek initially spurred appetite for risk as they did not drive up long-term US yields as feared, this had been reversed by the end of the week, as macro concerns resurfaced on the White House returning to a more aggressive stance on tariffs with several trading partners, hitting economically sensitive areas of the market the most.

Muted equity market activity also came ahead of the Q2 earnings season, which will officially kick off this week with large-cap US banks. In addition to these earnings reports, which serve as a barometer for US economic health and corporate activity, market attention will also focus on trade developments and inflation data for June. The latter will play a key role in shaping expectations for future rate cuts, where a benign inflation reading would support a risk-on mood, complementing low Q2 earnings growth expectations (S&P 500 Q2 +5.0%), which are being bolstered by exposure to the technology sector, a weaker USD, and a still-resilient US economy.

The Magnificent 7 took the lead again, rising by 0.6%

Fixed income

Fixed income performance was slightly negative last week, with investment grade (IG) and high yield (HY) down by 0.2%, while AT1s declined by 0.1%, partially offsetting the strong performances seen the previous week.

Yields on 10-year US Treasuries rose slightly last week and passed 4.4% on Wednesday, fuelled not only by concerns about future deficits, but also by a stronger focus on tariffs during the week. However, an auction of USD 39 billion of US Treasuries found strong demand and calmed the markets on Wednesday, which subsequently drove yields down.

In the UK, yields on 10-year gilts continued to rise and passed 4.6% on Wednesday. On top of worries about the UK budget, the Bank of England is now saying that a significant proportion of gilt investors are hedge funds, whose opportunistic positions are increasing the volatility of gilt prices.

The yield on 10-year US Treasuries has risen above 4.4%

Forex & Commodities

The USD consolidated over the last week, following the publication of stronger-than-expected US non-farm payroll data. Forex risk sentiment was largely unaffected by President Trump’s latest tariff proposals. The JPY weakened considerably following lower-than-expected Japanese wage growth data. The lack of wage growth means that the Bank of Japan will be in no rush to raise its deposit rate; the USD/JPY rose to levels above 146.

The USD/CHF failed to sustain its break below 0.79 and subsequently edged higher over the remainder of the week. Over the coming week, the main risk event for markets will be the publication of US CPI data. A higher-than- expected inflation print will lead to a modest USD consolidation, as markets may price out an imminent Fed rate cut.

Both gold and silver were largely rangebound last week, and they did not benefit from the return of tariff noise, suggesting that markets believe an extension of tariff deadlines will come about. Copper prices rose aggressively following Trump’s decision to place a 50% tariff on copper imports. We do not anticipate any further aggressive upside above USD 10,000 per tonne in the short term, given already abundant inventories.

A higher-than-expected inflation print will lead to a modest USD consolidation

The opinions expressed herein are correct as at 14 July 2025 and are subject to change without notice. This information should not be relied upon by the reader as research or investment advice regarding any particular fund, strategy or security. Past performance is not a guide to current or future results. Any forecast, projection or target, where provided, is indicative only and is not guaranteed in any way.