After the cautious investment cycle following the financial crisis, the first signs of increased capital expenditure globally will be particularly helpful for the large industrial segment within Swiss small & mid caps. Furthermore, Swiss small & mid caps have not quite reached the high levels of CFROI of their larger peers. With restructuring measures in place, increased sales dynamics being initiated and a greater focus on cash generation than in the past, the companies’ 2018 cash earnings growth potential is supported by both top-line growth and internal productivity measures.

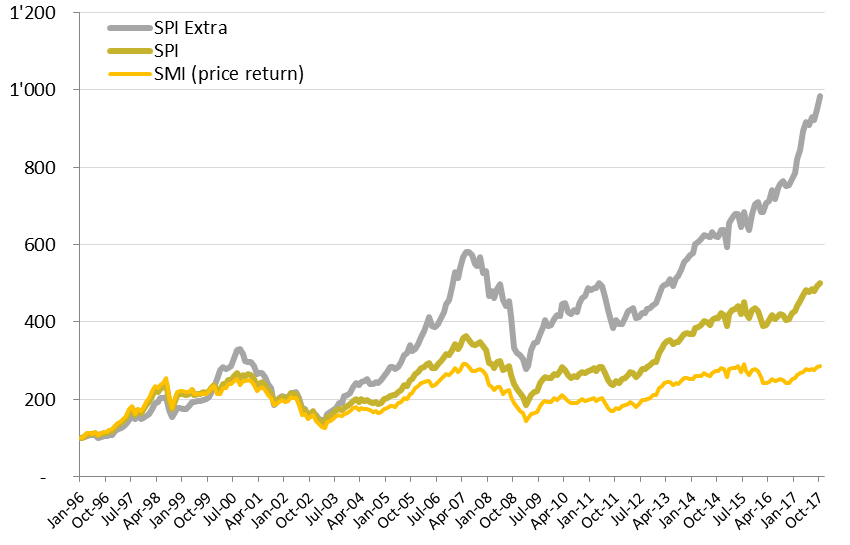

The SPI Extra, the Swiss index of stocks that are not members of the SMI (Switzerland’s top 20 stocks), has outperformed the SPI, the broad index, by no less than 315% since 1996. Performance after market corrections has lagged behind the wider index, following both the 2000 bubble and, more recently, the financial crisis. This recent slow development can almost certainly be attributed to the perceived high dependency on European export partners and the tepid investment cycle globally.

Comparative performance

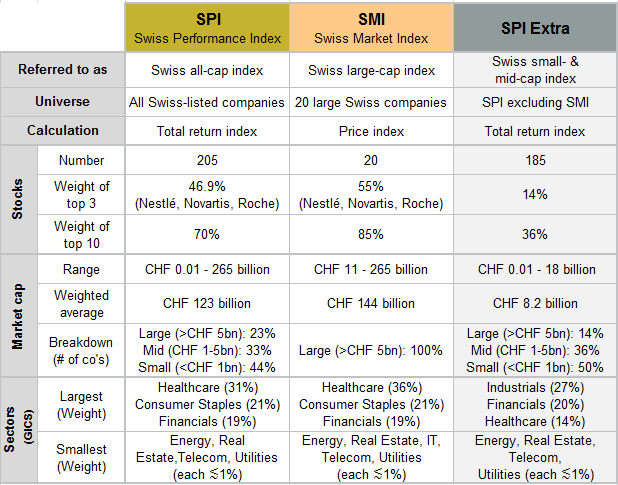

The SPI Extra attracts investors partly due to its lower concentration of risk than the broader SPI. Free of the three Swiss heavyweights, Nestlé, Novartis and Roche, the index offers a more balanced exposure to different sectors. Looking ahead to 2018, the largest sectors in the SPI Extra may benefit from the current stage of global economic growth: as mentioned above, industry from the investment cycle, and financials, supported by more activity, more loan growth and eventually by a gradual interest rate hikes in different countries.

Swiss indices comparison

Over the last two years, the SPI Extra has regained its historical premium to large caps. Currently, small- & mid-cap stocks are trading at a 12-month forward P/E ratio above 22x, while the SPI is trading just above 17x. The premium has been justified due to the long-term ability of Swiss small & mid caps to grow their earnings faster than their larger peers. Over 2017 and going into 2018, this is clearly the case. Not only have Swiss small & mid caps demonstrated stronger earnings growth than larger caps so far in 2017, but they have also been able to revise their guidance positively as the year progressed. Expectations for 2018 are higher than for larger caps, too, with earnings expected to grow in the mid-teens in the small- & mid-cap space, against a low-teen range for larger caps (excluding the one-off of reversing the effects of hurricanes).

Although the valuation ratios look extended, and are indeed above levels seen in recent history, it is interesting to note that the multiple expansion of Swiss small & mid caps has been less pronounced than that in neighbouring European countries. It seems reasonable to accept that the favourable economic environment does lead to an above-average multiple in general and it is pleasing that this remains modest in a relative context.

The Swiss small- & mid-cap space still has considerable room for improvement. EPS have not yet reached peak levels, potentially held back by the particularly severe currency headwinds, but also by the low level of investment since the financial crisis.

As regards currency, it important to remember that Swiss companies have successfully overcome a 40-year period of currency strengthening and the effects of the currency on companies are principally a translation, not a transaction risk.

EPS progression is a factor of improved sales levels and also improved profitability as a result of higher sales and internal productivity measures. These two factors should in turn support small- & mid-cap companies in catching up with the broader index in terms of CFROI levels.

Improving or maintaining high and stable CFROI is an essential factor in generating stock performance. Furthermore, it is this metric that best illustrates the operational abilities of a company. Understanding the evolution of CFROI in a company is how the team is able to identify successful investment opportunities for the portfolios the team manages.

The confidence that Swiss small- & mid-cap companies can generate improved operational performance and improve their CFROIs stems from a number of factors, for example, the geographical and sector exposure of the index should benefit from the current sustained growth trend globally.

High exposure to industrials, notably in added-value fields which tend to be more dynamic later in the cycle, is particularly attractive. A number of supply products being sold in Europe tend to be consumed as final products in emerging markets. Improving consumer demand, particularly in China, is very supportive. Indeed, looking that the final product and place of consumption, the geographical breakdown of Swiss small & mid caps is close to that of its larger peers, with a good 35% of them dependent on emerging markets. Subsectors and companies that come to mind would be automotive suppliers to German OEMs (Sika, Georg Fischer, Komax), technology component companies (VAT, Comet, AMS) and food ingredients (Hochdorf).

Small- & mid-cap companies in Switzerland continue to seek ways to improve productivity. A significant proportion of capital expenditure in recent years has been directed to upgrading production tools (Ypsomed comes to mind. It is reducing costs by building in East Germany and increasing productivity through more automation). Similarly, some engineering companies have reorganised themselves to become more customer-centric in order to avoid developing obsolete products (DormaKaba and Bobst, for example).

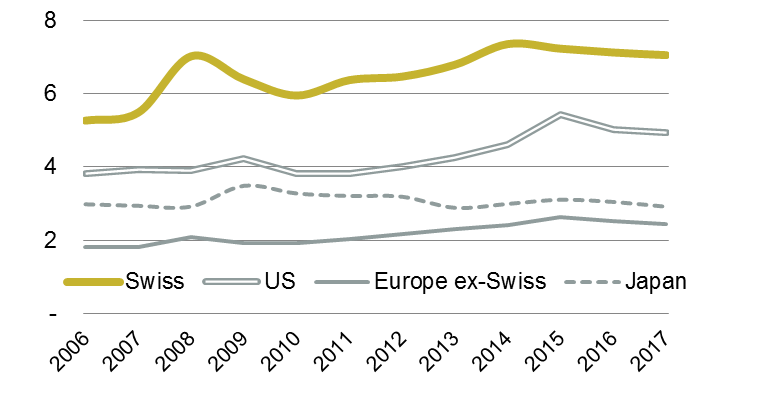

One of the more impressive characteristics of Swiss small & mid caps is their ability to adapt. A number of the companies in this segment have more than a hundred years of history. They have moved from being traditional Swiss industries that were facing international competition and adapted their product to new demands and new customers. Take the textile industry, for example: Oerlikon and Rieter have moved from serving local customers to adapting their respective products to the huge, competitive Chinese textile manufacturers. They have maintained their leadership in their respective fields and adapted prices, products and operational models to survive, remain profitable or regain profitability and seek out new growth markets. Similarly, Straumann adapted its range of products to address a growing price-sensitive customer base, without cannibalising its own high-performance products. Comet, despite controlling a vast share of the x-ray tube market globally, developed new technologies and created a new and growing market (which they also dominate) with their e-beam range. This adaptability is made possible by the traditionally high level of R&D spending that crosses the whole of the Swiss market, regardless of a company’s size. It is also supported by the high level of general education and support for higher education which is available in Switzerland.

Research & Development spend in major economies

In conclusion, the current macroeconomic environment is supportive of the performance of Swiss small- & mid-cap companies over the next 12 to 18 months. In the longer term, the adaptability, innovation drive and improvement potential of these companies should attract continued interest from investors.

Eleanor Taylor Jolidon

Co-Head Swiss & Global Equity

Martin Moeller

Co-Head Swiss & Global Equity