Five questions from the road...

Having spent the last two weeks travelling to see clients during what has been one of the most volatile periods in markets since the 2008 crisis irrespective of location, the questions and concerns most capturing clients’ attention were similar:

- Is high volatility here to stay?

- How much further will bond yields rise?

- How should bond investors manage the risk of rising rates?

- What do rising volatility and rising rates mean for equities?

- Why is the US dollar so weak?

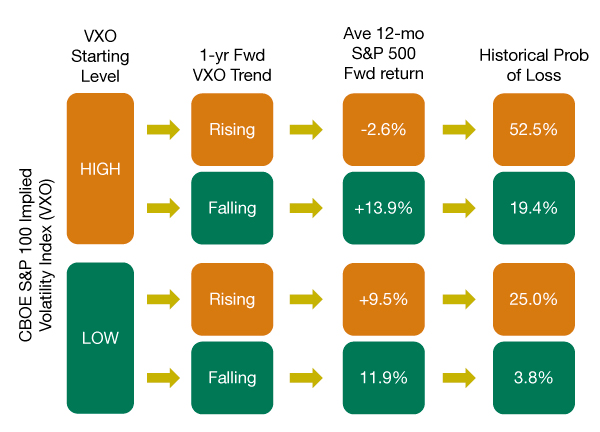

Is high volatility here to stay? YES

As we noted in our 2018 Outlook, falling volatility has been characteristic of the transition from economic crisis – such as the 1997-98 Asian/Russian crises, 2001’s bursting of the Tech bubble or the 2007-08 Global Financial Crisis – to recovery. In contrast, a stabilisation and rise in volatility is common in the late stages of post-crisis recovery. So with the US economy having transitioned from crisis to recovery and now, normalisation and as volatility settles just below historical averages, investors should acknowledge that a regime change in volatility has taken place from a low and falling regime to one that is low and rising. As seen going back to 1986, a low and rising volatility regime suggests a still relatively attractive return profile in equities though with a much greater risk of loss (chart) in equities looking ahead.

As a result of the pivot in volatility regime, we have begun implementing structured solutions in client portfolios more actively. Look back to the 2nd half of 2017, when volatility fell to all-time lows across many asset classes, we pivoted from selling volatility via structured product solutions to buying volatility via options to protect portfolios. With the return of volatility, we have unwound our options positions. While we will opportunistically seek options protection should conditions warrant, this new volatility regime suggests that conservatively designed structured product solutions will once again become a regular part of our implementation arsenal both to manage risk and support returns in client portfolios in the months ahead.

How much further will bond yields rise? 3-3.5% for US 10-year Yields in 2018

Most investors we have visited over recent weeks have focused their concerns on the prospect of higher interest rates and the outlook for rate hikes by the US Federal Reserve. Indeed, we believe the Fed remains on track to raise rates in March as well as another three times in 2018. Since the Fed began its rate hike cycle in late-2015, it has emphasised its desire to ‘normalise’ its policy settings in light of the recovery of the US economy following the 2008 Global Financial Crisis. Indeed, beginning with its tapering announcement in 2013, the Fed has been gradually guiding the real (adjusted for inflation) Fed Funds rate higher from the deeply negative levels seen in the post-crisis era to now, just short of zero (chart). A further four hikes in 2018, assuming an increase to near 2% core inflation, would leave real rates just above zero for the first time since 2008.

Rather than focusing only on changes in the Fed Funds rates, we have believed since early 2017 that investors should focus on the ‘normalisation’ process that had also begun in long-term government bonds. Much like with Fed Funds, following the crisis in 2008, the Fed, via its quantitative easing-driven purchases of US government bonds, pushed US 10-year yields adjusted for inflation down below zero in 2012. With its tapering announcement in 2013, real yields rebounded back to above zero though still below the levels seen both during the early stages of the crisis as well as compared to levels observed immediately prior to the 2008 crisis (chart).

With the rate hiking cycle combined with the shrinking of the Fed’s balance sheet, as with Fed Funds, the Fed appears to be guiding long-term rates progressively higher. Indeed, despite raising Fed Funds and rising long-term yields, the US economy is showing few signs that either is acting as an impediment to growth momentum. Moreover, with both the widening fiscal deficit due to the recently passed tax reform plan combined with the accelerating pace of shrinkage of the Fed balance sheet as additional catalysts, investors should expect the ‘normalisation’ process to continue in long-term yields. We expect them to move initially to the inflation adjusted ranges last seen during the first stages of quantitative easing, equivalent to nominal 10-year US Treasury yields of 3-3.5% by end-2018.

How should bond investors manage the risk of rising rates? Seek to diversify return drivers

Beginning in late-2016, we have focused our fixed income strategy on protecting against rising interest rates in favour of credit spread-driven returns. Investors have been rewarded for this focus with credit investors having realised strong returns driven by a decline in spreads from 200 bps to <100 bps despite a rise in risk free rates from their 2016 lows. While tight spreads are matched by strong corporate fundamentals – modest leverage, strong interest coverage, stable margins and improving cash flow – they similarly provide little cushion to offset the impacts of rising government bond yields on overall returns for investors. Moreover, while unclear when the cycle will turn and reverse the currently strong corporate fundamentals, what is plain is that the recent US tax reform measures will encourage the repatriation of cash and, either the deployment via dividends/ buybacks or increased capital spending. Both of these should drive an inflection of at least the leverage picture for American corporates – leverage is currently modest and had been falling. Those actions should drive leverage higher. For balanced investors, this has led us favour equity risk to fixed income within portfolios. However, for bond-only investors, the challenges are much more significant. Having managed interest rate risk down by pursuing short duration and floating rate strategies within the credit arena, we have also taken a more active manager approach to allow credit selection to drive returns more meaningfully relative to passive strategies which rely on declines in both interest rates and credit spreads.

Single-line bond held to maturity or fixed maturity portfolio strategies should likewise provide some shelter relative to fixed duration strategies common among many passive funds. With high yield bonds having performed exceptionally well through 2016-17, we began to diversify our exposure to other ‘high yielding’ bonds in mid-2017 to incorporate attractive carry vehicles such as Insurance-linked bonds and asset backed securities with less correlation to rising rates and/or widening credit spreads into portfolios. In addition, we began reintroducing alternative strategies with bond-like features such as merger arbitrage into portfolios, further reducing reliance on credit spreads as a driver to the ‘high yielding’ portions of our portfolios. For long-term investors in high yield bonds holding positions through the economic cycle, high yield bonds remain an attractive option. However, for shorter investment horizons, risk-reward warrants greater diversification of return drivers across the fixed income universe.

What do rising volatility and rising rates mean for equities? Focus on earnings to drive returns

Fortunately for equity investors, the US Federal Reserve has been overt in its communications about ‘normalising’ policy. As a result, corporates have taken the opportunity both to lock in low interest rates and extend the term of their borrowings, providing a cushion against near-term refinancing risks as well as most immediate negative impacts to earnings from rising rates. We do not therefore expect earnings to be negatively affected by the changing landscape in the US bond market while select sectors should benefit from the rising rate environment. However, the pivot in the volatility regime is likely to mean that expanding valuations which have served as a tailwind for equity returns in recent years will fade so forcing investors to rely on corporate earnings growth as the primary driver of returns. Indeed, since 2011, multiple expansion has accounted for almost half of the total returns generated by the S&P 500. In fact, even in challenging periods for the markets, such as 2015-16, multiple expansion served as the primary driver of returns while, with the return of earnings growth in 2017, multiple expansion still contributed nearly 7% of the 21% in the total returns generated by the S&P 500.

So, looking into 2018, rising volatility and rising interest rates should cap the contribution multiple expansion can make to investors’ total returns. However, with strong growth supported by recent tax reform, earnings growth of 15% should be sufficient to drive positive returns in US equities. While multiples likewise seem historically rich in emerging markets, strong earnings growth driven by economic recovery in Latin America and Eastern Europe combined with ongoing strength in Asian earnings should provide a more attractive risk-reward dynamic for global equity investors. Even as Japan sees more modest earnings growth of 9-10%, still historically low valuations provide an opportunity for not only earnings driven growth as seen in the US and Emerging Markets, but also the potential for a more sustained multiple expansion to support total returns for investors in 2018. As investors have increasingly pivoted their focus, rightly to the economy and corporate earnings, the spectre of trade wars and other geopolitical risks remains in the background and could move centre stage as we progress towards the mid-year. As such, equity investors should capitalise upon the rebound in volatility and seek to build capital protection into portfolios should these tail risk events transpire.

Why is the US dollar so weak?

Despite a persistent Fed and as of yet, more patient central bankers at the ECB and the Bank of Japan, the US dollar has weakened relentlessly since early-2017. However, it is worthwhile recognising the starting point from the US dollar weakness which was its value being the most expensive in real effective exchange rate terms (chart) since the Plaza Accords devaluation of the US dollar in 1985.

While most (including ourselves) have focused on the widening interest rate differential between the US dollar and other key currencies around the world, 2017 saw a number of important inflections in key drivers which are now weighing upon the US dollar. Perhaps the most visible was the early-2017 surprise in European economic growth which left eurozone real GDP growth rates at a premium to US growth rates for the first time since 2011, near the start of the bull market in the US dollar.

Moreover, whereas during the 2011-16 bull market in the US dollar, underlying economic fundamentals tilted in favour of the greenback from 2017 onwards, those same fundamentals are now proving to be headwinds to US dollar strength. The US budget deficit which had troughed at nearly 10% of GDP at the depths of the Global Financial Crisis in 2009 narrowed to 2% of GDP in 2015. While eurozone fiscal deficits widened to 6% of GDP during the crisis and narrowed again as recovery took hold, the single currency area only succeeded in closing its budget gap to a comparable 2% of GDP in 2015. In 2017, the eurozone economic recovery and fiscal prudence allowed its budget deficit to narrow further to 1% of GDP. In contrast, the inability of US President Donald Trump to deliver fiscal restraint continued to push the US fiscal deficit out further to 3.4% by end-2017, even before the implementation of the tax reform plan passed in December. With the tax reform plan expected to expand the deficit to as much as 5-6% of GDP by 2019, a further headwind for the US dollar lies ahead. This was further compounded by the introduction of the Chinese Yuan into the IMF Special Drawing Rights (SDR) basket and a shift from a managed US dollar-referenced rate to one managed against the broader SDR basket incrementally increasing the suitability of Yuan investment for central banks in particular looking to diversify US dollar-heavy positions. The potential to ‘price’ this deterioration in the US dollar has weakened and interest rates have begun to rise in the US leaving the differential between US dollar rates and German counterparts as nearing the widest seen since the late-1990s.

Tactically, one-sided positioning against the US dollar combined with the wide interest rate differential suggest a reversal in the US dollar weakness of the past year may be in the offing supported by renewed political uncertainty in Europe (Italian elections/German coalition), a delay in the expected September start to ECB ‘tapering’ of its quantitative easing programme, and/or a relapse in eurozone growth momentum relative to the US.

Michaël Lok

Group CIO and Co-CEO Asset Management

Norman Villamin

CIO Private Banking

Patrice Gautry

Chief Economist