Key points

- The relief felt by markets following the US tariff announcement may be short-lived

- Recent moves on tariffs signal the start of the next, more challenging phase of the Trump presidency

- Risks of further sustained US dollar weakness and persistently elevated volatility

- Investors should look to increase exposure to capital protected and hedge fund strategies

Markets breathed a sigh of relief following the announcement of US tariffs on steel and aluminum which included exemptions for Canada and Mexico, two of the largest steel exporters to the US and with whom the US is currently renegotiating the North American Free Trade Agreement (NAFTA).

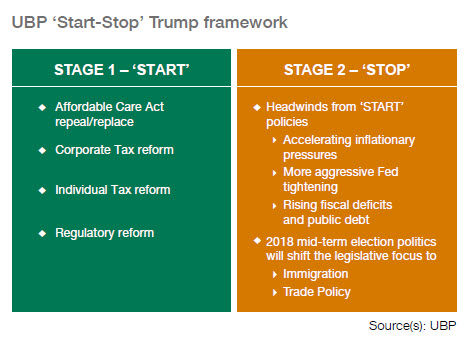

In the near term, this brings reassurance that an immediate trade confrontation is not set to flare up. Such a development might have signalled an unwelcome end to the trilateral trade bloc created in 1994. However, the series of tariffs implemented since the start of the year – covering lumber, airplanes, washing machines, solar panels and now steel and aluminum – confirms a pivot from the ‘Start’ stage of the UBP ‘Start-Stop’ framework (for more details see Spotlight: Navigating a Trump Presidency, February 2017) to the more challenging ‘Stop’ phase.

The ‘Start’ phase stimulated economic growth, driven by regulatory reform and culminated in the announcement of tax cuts in December 2017. The transition to a ‘Stop’ phase has been visible since January 2018 with accelerating inflationary pressures, a more aggressive tone to Fed interest rate policy combined with rising fiscal deficits in the United States.

As we enter campaign season ahead of the November 2018 Congressional elections, we expect the economic focus of the ‘Start’ phase should more meaningfully give way to the politically focused components of the ‘Stop’ phase. The more confrontational trade policy seen in recent weeks is likely to be only the beginning. With Canada and Mexico now exempt, the burden of US steel and aluminum tariffs falls mainly on Europe, Korea, Japan, Russia, Brazil and China. The EU and China have already indicated that they intend to retaliate with their own tariffs.

In the near term, given the strength not only of the US economy – with the US ISM survey signalling corporate confidence at 13-year highs and consumer confidence near 14-year highs – as well as the strength of other major economies around the world, it would take a broaderbased shift in global trade policy to stall growth momentum significantly. However, with retaliation potentially on the way from the EU and China, should the US continue to take a hard line in North American Free Trade Agreement (NAFTA) negotiations, a victory by the populist presidential candidate in Mexico’s July elections could trigger a formal withdrawal by the US or Mexico from the free trade agreement. A course of action like this would remove the key obstacles to a much more direct trade confrontation within North America.

In addition, though Chinese steel and aluminum exports are a modest US$700m, the completion of a US investigation into Chinese compliance with intellectual property rights agreements looks set to complete over the summer. This also raises the potential for a more significant trade stand-off between the world’s two largest economies.

For investors, the most immediate risk as markets seek to price a less open global trading regime will be via the US dollar. It is worth looking back for a precedent to the 1980s and 1990s when the US and Japan, then the two largest economies in the world, regularly sparred over trade. Even following the 1985 Plaza Accord which devalued the US dollar against major trading partners, the then US President Ronald Reagan’s trade policies against Japan were followed by subsequent actions by President Bill Clinton culminating in 100% duties on imports of Japanese autos in 1995.

With a German coalition having been formed and a hung parliament in the Italian elections, the near-term threats to a sharp weakening in EURUSD appear to have passed. Though a delay to the expected tapering by the European Central Bank as well as historically large speculative positioning against the US dollar remain potential headwinds, the trajectory on trade suggests that medium-term US dollar weakness lies ahead.

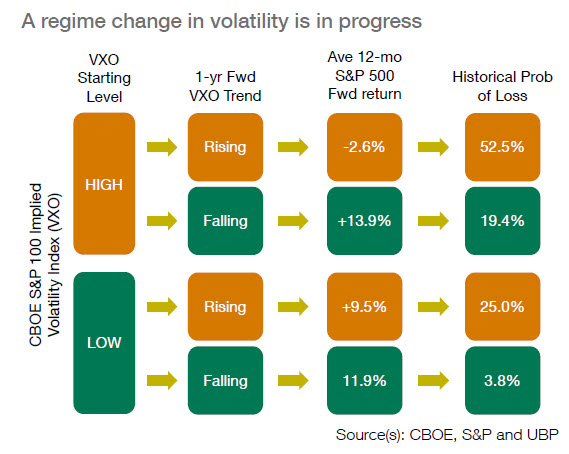

The pivot to the ‘Stop’ phase of the UBP Trump framework also confirms the regime change in volatility highlighted in the UBP 2018 Investment Outlook. The beneficial low-falling volatility regime that characterised the strong market returns in 2017 has given way to a low, but rising regime in early 2018.

Historically, this has meant that while investors should be more wary of losses in volatile markets, the one year return profiles have remained attractive at near 10% in the S&P 500 (illustration). However, should the pivot to the ‘Stop’ phase entail a more significant trade confrontation, a shift from low and rising volatility may give way to a more harmful high and rising volatility regime where risk-reward tilts meaningfully against investors.

As a result, while the recent announcement on tariffs from the US has calmed markets, investors should use this as an opportunity to pivot portfolios to protect against the regime change - from ‘Start’ to ‘Stop’ - in the Trump presidency. At the same time, it would be wise to acknowledge the risks of a potential further regime change in volatility.

While bond investors have focused much of their risk management on reducing interest rate risk in fixed income portfolios, given the tightness of credit spreads, we believe it is time for investors to pivot their risk management efforts towards credit portfolios as well. In recent months, we have diversified our ‘high yielding’ bond exposure to include insurance-linked, asset backed securities and emerging market local currency debt exposure to reduce our reliance on US and European credit spreads to drive returns within portfolios. Increasingly, looking forward, we will look to non-US dollar, non-directional bond and hedge fund strategies to further diversify return drivers within fixed income portfolios.

Though the strong economic and earnings backdrop continues to favour equities over bonds, the shift in volatility regime means that opportunities are emerging in structured products to provide elements of capital protection into portfolios while still allowing for upside participation that we expect in equities. Moreover, volatility dampening strategies in the hedge fund arena offer investors growing opportunities to secure less directional exposure in equities, much like we have done in fixed income throughout 2017.

Michaël Lok

Group CIO and Co-CEO Asset Management

Norman Villamin

CIO Private Banking

Patrice Gautry

Chief Economist